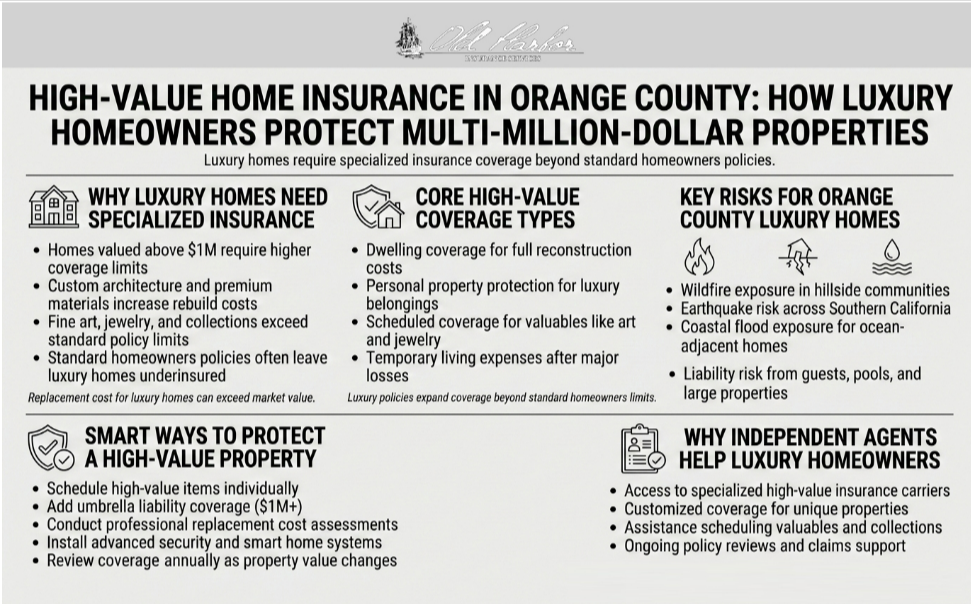

Orange County luxury properties exceeding $1 million demand specialized insurance that standard policies simply don’t provide. Custom architectural features, fine art collections, and high-end amenities require tailored coverage most homeowners overlook. Generic policies leave these properties severely underinsured. That’s why partnering with a local independent agent like Old Harbor Insurance is essential.

This comprehensive guide reveals exactly what luxury homeowners need to know about high-value coverage, specialized risks, and proven strategies. Keep reading to discover how customized insurance transforms protection into genuine financial security.

Understanding High-Value Home Insurance vs. Standard Policies

Luxury homes require fundamentally different insurance approaches than standard properties. A $1.5 million Orange County home’s replacement cost often far exceeds its market value. Standard policies cap dwelling coverage at preset limits that leave luxury properties severely underinsured.

High-value policies account for custom architectural features, premium building materials, and specialized labor required for luxury reconstruction. Understanding this distinction is essential for adequate protection.

What High-Value Coverage Actually Includes

Dwelling and Structural Protection

High-value dwelling coverage protects your home’s complete structure including custom features, upgraded HVAC systems, smart home infrastructure, and architectural elements. Unlike standard policies with fixed limits, luxury coverage expands to reflect your home’s actual reconstruction cost. Accurate dwelling limits are non-negotiable for Orange County estates.

Your coverage should account for premium materials, specialized contractors, and architectural details unique to your property. Working with an agent who conducts detailed replacement cost analyses ensures your dwelling limit matches today’s construction prices.

Personal Property and Valuables Scheduling

Personal property coverage in standard policies typically maxes at 50-70% of dwelling limits—insufficient for fine art or jewelry. High-value policies allow individual scheduling of valuable items with full coverage. Scheduled items bypass policy restrictions—your $150,000 painting gets full coverage, not a $2,500 cap.

Enhanced Liability Protection

Standard liability coverage of $100,000-$300,000 becomes inadequate for luxury estates hosting gatherings or featuring pools. High-value policies provide $1 million or higher in liability protection, with umbrella policies adding $2-5 million. This layered approach protects your assets if someone is injured on your property.

For Orange County’s high-net-worth residents, this protection is essential given the region’s litigious environment.

Additional Structures and Specialty Amenities

Guest houses, detached garages, pools, and tennis courts require individual coverage consideration. High-value policies extend coverage to these structures with higher limits. Specialized endorsements protect pool liability or equipment breakdown.

Understanding how your specific amenities are protected prevents gaps when claims occur.

High-Value vs. Standard Coverage Comparison

| Coverage Component | Standard Homeowners Policy | High-Value/Luxury Home Policy |

| Dwelling/Structure | Basic rebuild cost limits | Higher rebuild cost with extended limits |

| Personal Property | ~50% of dwelling limit | Custom scheduled items (art, jewelry, collections) |

| Liability Protection | $100,000–$300,000 | $1 million+ with umbrella options |

| Additional Structures | Covered at % of dwelling | Higher optional limits for specialty buildings |

| Flood/Earthquake | Usually excluded | Add-ons/standalone policies available |

| Endorsements | Limited options | Wide range (smart tech, identity theft, equipment breakdown) |

Orange County-Specific Risk Factors for Luxury Homes

Coastal Properties and Flood Exposure

Orange County’s coastal and low-lying luxury homes face significant flood risk from heavy rainfall and storm surge. Standard homeowners policies explicitly exclude flood damage—leaving multi-million-dollar coastal estates completely unprotected. The National Flood Insurance Program provides coverage through separate policies, though private flood insurance offers higher limits for luxury properties.

The County of Orange Flood Insurance information details local flood zones and requirements. Discussing flood risk with your agent determines appropriate coverage for your location.

Earthquake Risk and Specialized Coverage

California’s seismic activity makes earthquake insurance a serious consideration for Orange County luxury homes. California earthquake insurance requires separate policies since standard coverage explicitly excludes seismic damage. The California Earthquake Authority provides coverage through participating carriers tailored to high-value properties.

Earthquake premiums for luxury homes vary based on location, construction type, and deductible selection. Professional guidance ensures appropriate coverage for your specific situation.

Wildfire Risk and Market Availability

Orange County’s proximity to wildfire zones affects insurance availability and pricing for upscale properties. Standard policies cover fire damage, but verification of adequate limits is essential for properties in elevated areas. Some carriers require additional endorsements or impose higher deductibles in high-fire-risk zones.

When private insurers deny coverage, the California FAIR Plan serves as an insurer of last resort. However, FAIR Plan coverage is limited and premiums run significantly higher than standard rates.

Questions Luxury Homeowners Should Ask Their Agent

Are contents covered at replacement cost or actual cash value? How are valuables scheduled and appraised? How will rebuilding costs reflect unique architectural work? What deductibles apply for different perils? Is flood coverage included or separate? Do liability limits match your risk profile?

Endorsement and Claims Questions

Are there specialized endorsements for smart home systems, cyber protection, or equipment breakdown? How does the claims process work for high-value losses? What documentation is expected during adjustment?

Understanding Luxury Home Insurance Costs

Replacement Cost vs. Actual Cash Value

Replacement cost covers full current prices for rebuilding, while actual cash value depreciates items over time. For luxury homes, replacement cost is essential—it ensures your kitchen renovation gets full coverage. Higher coverage limits increase premiums, but they reflect genuine protection.

Premium Factors Specific to High-Value Properties

Home condition and materials significantly impact luxury home premiums. Fire-rated roofing, upgraded electrical systems, and excellent maintenance reduce premiums. Security systems and smart home monitoring also trigger insurance discounts.

Avoiding Underinsurance: A Practical Checklist

Luxury homes become underinsured when valuations don’t reflect current rebuild costs or content values aren’t updated regularly. Conducting a detailed home inventory with professional photos and appraisals prevents these gaps. Document all valuables, collections, and special features with annual reviews to ensure coverage keeps pace with property improvements.

Market Trends Impacting Luxury Coverage in Orange County

Research from the Terner Center at UC Berkeley shows California’s home insurance market facing increased pressure from rising catastrophe risk and climate change. These trends force insurers to adjust pricing—especially for high-value properties in exposed areas.

Understanding these trends helps luxury homeowners anticipate market changes. Independent agents with market expertise help navigate shifts and secure the best available options.

How Independent Agents Serve Luxury Homeowners

Access to Specialized High-Value Carriers

Independent agents represent carriers specializing in high-value properties—companies with expertise in luxury coverage, valued at millions, and complex risk profiles. These carriers offer tailored solutions that standard market insurers simply don’t provide.

Old Harbor Insurance brings deep knowledge of Orange County’s luxury markets. We understand which carriers excel in your specific neighborhood and risk profile. This expertise saves time and ensures you access the best available options.

Customized Coverage Planning

Beyond securing coverage, independent agents conduct thorough assessments of your situation. They evaluate your home’s unique features, lifestyle, and risk exposure. This customized approach prevents both underinsurance and overpaying.

Your agent becomes a long-term partner, reviewing coverage annually and adjusting as your property evolves.

Claims Support and Advocacy

When a loss occurs, independent agents provide expert support that direct insurers can’t match. Your agent guides documentation, communicates with adjusters, and advocates for fair treatment. This partnership approach is invaluable during high-value claims where stakes are significant.

How Old Harbor Insurance Serves Orange County Luxury Homeowners

At Old Harbor Insurance, we understand that luxury properties demand more than standard coverage and generic service. We invest time thoroughly understanding your specific circumstances, property details, asset values, and risk exposures before recommending coverage. Our independent approach means we shop specialized carriers on your behalf.

We’ve helped hundreds of Orange County affluent homeowners navigate complex insurance decisions. Our agents understand luxury markets and know which carriers excel at high-value claims. See what luxury homeowners say about working with Old Harbor Insurance.

Protect Your Luxury Orange County Investment

Securing proper coverage for your luxury home shouldn’t require months of research or settling for inadequate options. One conversation with an Old Harbor Insurance agent reveals coverage gaps and options you didn’t realize existed. Get a personalized quote in minutes, and we contact you within 24 hours with recommendations.

Call (951) 297-9740, email info@oldharbor.com, or schedule a consultation. Your luxury property deserves expert protection from a team that understands high-value coverage.

Frequently Asked Questions

What makes a property “high-value” for insurance purposes?

Properties exceeding $1 million in value typically qualify as high-value. Custom architecture, premium materials, and significant valuables all indicate the need for specialized coverage beyond standard policies.

How much should my dwelling coverage be for a luxury home?

Dwelling coverage should reflect your home’s full replacement cost in today’s market. Annual appraisals or professional analyses ensure your limits keep pace with construction cost inflation.

Can I get earthquake and flood coverage for my Orange County luxury home?

Yes. Earthquake coverage is available through the California Earthquake Authority or private insurers as separate policies. Flood coverage comes through the National Flood Insurance Program or private carriers offering higher limits than NFIP maximums.

What’s the difference between scheduled and unscheduled personal property coverage?

Unscheduled coverage limits high-value items to sublimits (often $2,500 per item). Scheduled coverage lists specific valuables with individual appraisals, providing full coverage. For luxury homeowners with art or jewelry, scheduling is essential.

How does a higher deductible affect my luxury home premiums?

Higher deductibles lower monthly premiums but increase out-of-pocket costs during claims. Many luxury homeowners use the “1% deductible rule”—selecting deductibles representing 1% of dwelling coverage limits.

What specialized endorsements should a luxury home have?

Consider equipment breakdown for smart systems, cyber protection for connected devices, loss assessment for community fees, and specialty endorsements for pools or guest homes. Your agent recommends endorsements matching your specific amenities.

How often should I review my luxury home insurance coverage?

Review annually and after property improvements or lifestyle changes. Market conditions shift and new carriers enter markets, so annual reviews ensure your coverage remains adequate.

What happens if private insurers won’t cover my luxury property?

The California FAIR Plan provides fire-only coverage up to $3 million when private markets won’t insure properties. However, FAIR Plan premiums typically run 30-50% higher. Proactive planning prevents coverage crises.