Most Chula Vista homeowners don’t realize they’re paying hundreds more than necessary for home insurance. Between aggressive rate increases from national carriers, difficulty finding coverage in high-risk ZIP codes, and confusion about what policies actually cover, getting fair pricing feels impossible. That’s where working with an independent agent like Old Harbor Insurance makes all the difference.

Here’s what might surprise you: the homeowner next to you could be paying significantly less annually—not because their home is different, but because they’re shopping smarter. Keep reading to discover where those savings actually hide.

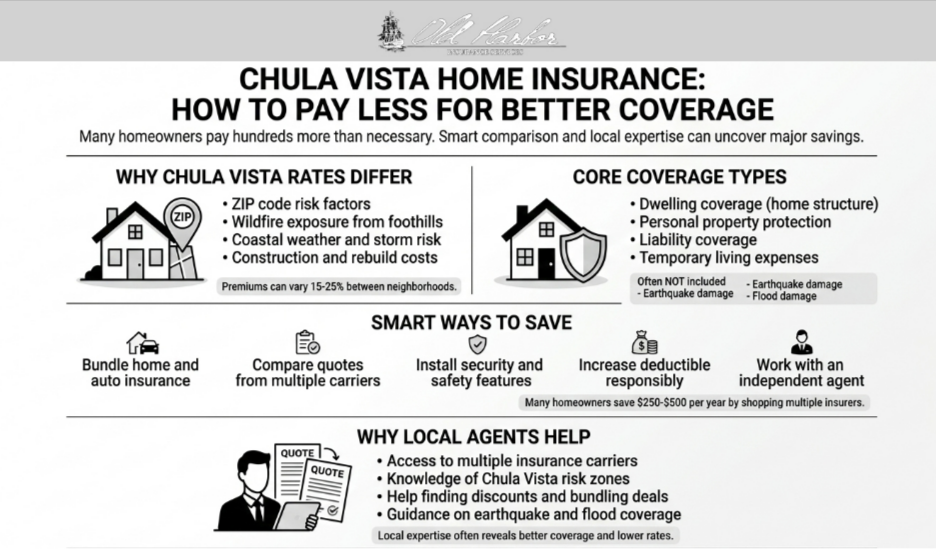

Why Chula Vista Homeowners Face Unique Insurance Challenges

Chula Vista’s location in San Diego County creates a perfect storm of insurance risk factors. You’re dealing with coastal exposure, wildfire risk from inland foothills, seismic activity, and flood potential—especially in ZIP codes near the Sweetwater River and Otay Ranch areas.

According to California Department of Insurance data, San Diego County has seen significant shifts in insurer participation over the past five years. Some carriers have exited the market entirely, while others have raised rates dramatically in specific neighborhoods. This creates both challenges and opportunities for savvy homeowners.

How ZIP Code Shapes Your Insurance Rate

Your ZIP code is one of the single biggest factors determining your premium. Insurance companies assess local risk patterns—crime rates, fire exposure, flood history, and construction costs—at a granular level.

In Chula Vista, rates can vary 15-25% between neighborhoods based on these factors. Properties in lower-risk zones qualify for better rates, while coastal and wildland interface areas face increases reflecting actual fire exposure. An independent agent who knows these patterns identifies which carriers price competitively in your specific location. The difference between shopping blind and shopping with expertise often means finding $300-500 in annual savings.

Understanding Your Home Insurance Coverage

According to the California Department of Insurance’s residential insurance guide, every homeowner should understand their policy’s core coverage components. Let’s break down what actually protects you in Chula Vista.

Dwelling Coverage: The Foundation

Dwelling coverage protects your home’s structure—walls, roof, foundation, garage, and built-in systems. Your dwelling limit should reflect replacement cost, not market value. In Chula Vista’s market, construction costs run higher due to labor and specialty materials.

If your $400,000 home has only $250,000 in dwelling coverage, you’re severely underinsured. That gap means you pay reconstruction costs beyond your policy limit.

Personal Property and Liability

Personal property coverage protects furniture, appliances, electronics, and clothing. This typically maxes out at 50-70% of your dwelling limit. Liability coverage protects you if someone is injured on your property or you accidentally damage theirs—critical protection given Chula Vista’s active outdoor lifestyle with pools and frequent gatherings.

Earthquake and Flood Coverage

Standard homeowners policies exclude earthquake damage. The California Earthquake Authority provides earthquake insurance as a separate policy for California homeowners. Given Chula Vista’s proximity to fault zones, this coverage is a prudent add-on. Similarly, standard policies don’t cover flood damage. The National Flood Insurance Program offers coverage through separate policies when private market options are limited.

The Independent Agent Advantage in Chula Vista

Access to Multiple Carriers

Independent insurance agents represent numerous carriers, allowing them to compare rates and coverage from multiple companies simultaneously. Unlike captive agents who offer only single-insurer options, independent agents have access to dozens of carriers tailored to different risk profiles.

This competitive shopping process often uncovers 20-30% savings compared to direct insurer quotes. When you work with Old Harbor Insurance, our agents know which carriers price competitively in Chula Vista and which ones to skip entirely. We maintain relationships with A-rated carriers across California, ensuring you get quotes only from financially stable, reliable companies.

Personalized Local Expertise

Independent agents take time understanding your specific needs, property details, and budget. They assess your home’s age, construction materials, safety features, and local risk factors before recommending coverage. This personalized approach ensures you’re neither underinsured nor overpaying for unnecessary coverage.

You provide your information once, and your agent shops on your behalf across multiple companies. This saves considerable time and effort while identifying discounts you’d likely miss shopping alone. Many homeowners are shocked to discover they qualify for discounts they never knew existed—from security system savings to bundling rewards to loyalty incentives.

Proven Strategies to Lower Your Chula Vista Home Insurance Costs

Bundle Policies for Maximum Savings

Bundling homeowners and auto insurance through the same company reduces your overall premium by 11-15%. Independent agents compare bundled pricing across multiple carriers to ensure you’re getting the best combined rate available.

Shopping bundled packages with professional guidance often reveals savings that direct shopping misses. Your agent identifies which carriers offer the best bundling discounts for your specific profile in Chula Vista.

Maximize Available Discounts

Insurance companies offer numerous discounts for safety features like storm-resistant roofing, updated electrical wiring, alarm systems, and clean claims histories. Some offer discounts for good credit scores or annual premium payments. Your independent agent knows which carriers offer the best discounts for your situation.

Compare Multiple Quotes

Don’t settle on the first quote you receive. Comparing quotes from at least three different carriers reveals significant price variations. Research shows homeowners save an average of $250 per year by shopping around with professional assistance.

Special Considerations for Chula Vista Properties

Wildfire and Coastal Storm Risks

Chula Vista’s proximity to wildfire zones and coastal exposure make fire and wind damage particularly relevant. Your dwelling coverage should reflect current rebuild costs, which typically run higher in coastal San Diego County. Some insurers may require specific safeguards—like defensible space maintenance or wildfire risk mitigation measures—in high-fire-risk ZIP codes.

Research from the Terner Center at UC Berkeley shows California’s home insurance market has shifted dramatically, with rising premiums and insurer exits affecting availability. Understanding these trends helps you anticipate future rate changes in Chula Vista.

When Traditional Coverage Falls Short

Some Chula Vista properties struggle finding traditional market coverage due to high-risk classifications. The California Department of Insurance FAIR Plan provides coverage when private insurers deny applications. Independent agents help navigate these scenarios and identify specialty markets that other agents might not know about.

How Old Harbor Insurance Helps Chula Vista Homeowners

At Old Harbor Insurance, we listen to understand your circumstances completely. We don’t just quote rates—we educate you on all insurance options available to your specific situation. Our independent agent network across California navigates complex state regulations like California Proposition 103 to ensure you’re getting compliant rates and maximum consumer protections.

We’ve helped hundreds of homeowners in San Diego County find better rates and comprehensive protection. Our clients appreciate the transparency, personalized service, and genuine care we bring to every quote and claim—see what they have to say.

Your Protection Starts Here

Protecting your Chula Vista home shouldn’t mean navigating confusing paperwork or spending hours on hold. Our independent agents streamline the entire process, uncovering coverage options you’ve never heard of and discounts that add up fast. Get a free quote in just minutes—we’ll contact you within 24 hours with personalized recommendations tailored to your property.

Ready to get started? Call (951) 297-9740, email info@oldharbor.com, or talk to our team. Better coverage, smarter pricing, and genuine peace of mind are waiting.

Frequently Asked Questions

What’s the average cost of homeowners insurance in Chula Vista?

Costs vary significantly based on ZIP code, home age, and risk factors. Coastal areas and high-fire-risk zones typically see higher premiums than inland neighborhoods. An independent agent can provide accurate quotes for your specific property.

Do I need earthquake insurance if I live in Chula Vista?

Yes, it’s highly recommended. Standard homeowners policies exclude earthquake damage, and California’s seismic activity makes this coverage a prudent safeguard for most properties. Your agent can explain coverage options and costs.

How much dwelling coverage should my Chula Vista home have?

Your coverage should reflect replacement cost, not market value. Account for Chula Vista’s higher construction costs and any detached structures. An independent agent can calculate appropriate limits based on your home’s specifications.

Will increasing my deductible really save me money?

Absolutely. Higher deductibles mean lower premiums—but only choose amounts you can comfortably pay out-of-pocket if you need to file a claim. Your agent helps you find the right balance.

Should I bundle my homeowners and auto insurance?

Bundling typically saves 11-15% on combined premiums when rates are competitive across policies. An independent agent compares bundled pricing across multiple carriers to ensure you’re getting the best deal.

What home improvements can lower my insurance rate?

Safety features like alarm systems, fire-resistant roofing, updated electrical wiring, and storm-resistant upgrades often qualify for discounts. Maintaining defensible space around your property helps in high-fire-risk areas. Ask your agent which specific improvements carriers in your area reward.

How often should I review my homeowners insurance policy?

Review coverage annually or after major life changes like home improvements, renovations, or significant property purchases. Market rates change frequently, and your agent can identify new savings opportunities and coverage adjustments you might need.