Laguna Hills homeowners face unique insurance challenges shaped by hillside location, wildfire proximity, and earth movement risk. Many residents discover their standard homeowners policies leave critical gaps unprotected. Old Harbor Insurance works with Laguna Hills residents to find coverage tailored to hillside-specific risks.

In this guide, we’ll walk you through what home insurance covers in California, what specific risks threaten Laguna Hills properties, and why a local independent agent beats going it alone. You’ll understand the threats, your coverage options, and how to protect your hillside investment.

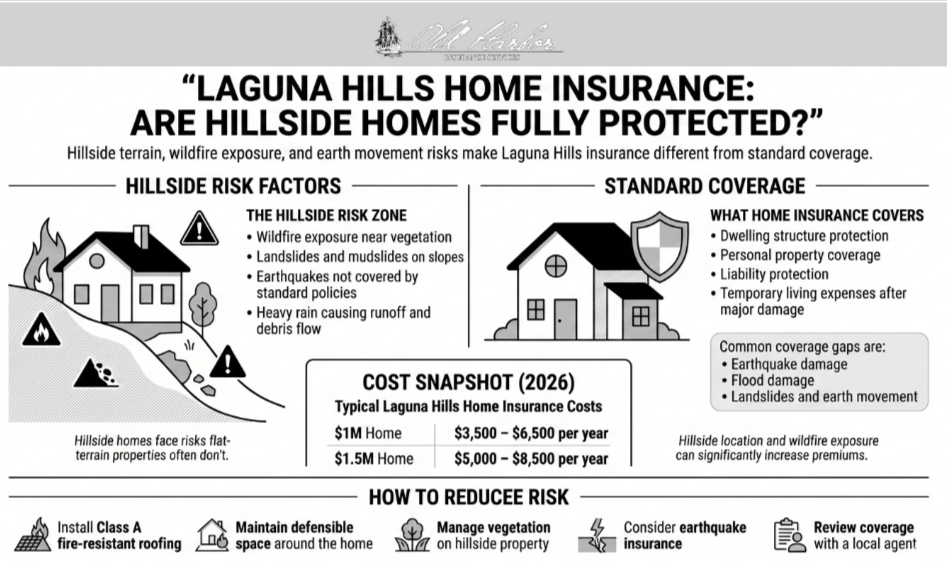

The Laguna Hills Home Insurance Challenge

Laguna Hills sits on Orange County’s hillside terrain, creating multiple insurance challenges most residents don’t anticipate. Wildfire exposure is significant—homes near wildland interfaces face increasing scrutiny from carriers. Earth movement risks including landslides and mudslides add complexity that flat-terrain properties don’t face.

The California insurance market has tightened significantly, and hillside properties experience this pressure more acutely. The UC Berkeley Terner Center shows how climate risks are reshaping insurance, particularly for hillside and fire-adjacent properties.

Understanding Hillside-Specific Risks

Laguna Hills hillside properties face unique hazards that standard homeowners policies often don’t adequately address. Wildfire risk is the primary concern—homes near wildland interfaces face significant exposure. Earth movement risks including landslides, mudslides, and sinkholes add another layer of complexity specific to slope properties.

The California Department of Insurance tracks wildfire risk data showing loss patterns and premiums for homes in high-risk areas. This government-reported data directly influences how carriers assess and price hillside properties.

Wildfire Risk in Laguna Hills

Wildfire risk has become the primary factor affecting insurance availability and pricing for hillside Orange County homes. Homes on slopes with vegetation exposure and wind patterns face different underwriting than valley properties. The California Department of Insurance’s Wildfire Risk Reporting explains regulatory requirements for insurers to track fire loss data by ZIP code.

The good news? Practical mitigation steps can reduce risk and potentially lower premiums: ember-resistant zones, fire-resistant roofing, and vegetation management around your home. Many carriers offer 5-15% discounts for verified mitigation work.

Landslide, Mudslide, and Earth Movement Risks

Hillside properties face earth movement risks that flat-terrain homes don’t experience. The California Department of Insurance’s Flood, Mudflow, and Mudslide Fact Sheet explains how homeowners insurance treats landslides, mudflows, and sinkholes. Coverage varies significantly based on the cause and type of earth movement.

Earth movement events often have special coverage rules requiring careful policy review. If your home sits on a slope or near unstable terrain, understanding these coverage gaps is essential.

Landslide vs. Mudflow vs. Debris Flow: Why Coverage Depends on the Cause

Not all earth movement is treated the same by insurers, and the distinction matters enormously for Laguna Hills homeowners. A dry landslide is typically excluded under standard homeowners policies as “earth movement.” A mudflow caused by heavy flooding may be covered under a flood policy through NFIP. Debris flow following wildfire has coverage that depends on whether the triggering event was fire or flood.

Many homeowners assume they’re covered only to discover after a loss that the cause determines the payout. Understanding these distinctions helps you identify critical coverage gaps before disaster strikes.

Earthquake Coverage: Essential for Laguna Hills

Earthquakes aren’t covered by standard homeowners insurance in California—a critical gap for Laguna Hills residents in a seismically active region. Earthquake insurance must be purchased separately and comes with deductibles typically 15-20% of your coverage limit.

For a $2 million hillside home, that could mean a $300,000-400,000 deductible. This decision requires professional guidance because earthquake risk is real, but the cost must be weighed carefully.

Flood Insurance: Don’t Assume You’re Protected

Standard homeowners insurance does not cover flood damage—a complete exclusion for all properties. For Laguna Hills hillside homes, flood risk comes from heavy rainfall, debris flows during intense storms, and emergency water runoff during fire events.

Flood insurance is required by mortgage lenders if your property is in a FEMA flood zone. If you’re outside a mapped zone, it’s optional but highly recommended given Laguna Hills’ hillside terrain and storm exposure.

2026 Laguna Hills Hillside Home Insurance Cost Snapshot

Home insurance pricing in Laguna Hills varies significantly based on hillside exposure, wildfire risk, earth movement vulnerability, and home age. Most homeowners fall into predictable ranges adjusted for hillside location and risk.

| Rebuild Value | Standard Policy | Hillside & Fire Exposure | With Earthquake Add-On |

| $1,000,000 | $3,500–$6,500/year | $5,500–$9,500+ | $2,000–$4,500 |

| $1,500,000 | $5,000–$8,500/year | $8,000–$13,000+ | $3,000–$6,500 |

| $2M+ | $7,000–$14,000/year | $11,000–$20,000+ | $4,500–$8,500 |

What Drives Hillside Property Premiums?

Hillside location significantly impacts pricing—slopes with vegetation exposure and wind patterns face higher rates. Roof age matters enormously; older roofs trigger premium increases while Class A fire-resistant roofing qualifies for discounts.

Distance from wildland interface, vegetation management around your home, and documented fire mitigation work all affect your final price. Earth movement exposure, prior claims history, and deductible structure also influence premiums substantially.

Why Rebuild Costs Are Higher on Hillsides

Rebuild cost on Laguna Hills slopes exceeds $450-650 per square foot depending on engineering requirements—significantly higher than flat-terrain properties. Sloped lots increase construction difficulty, narrow roads limit equipment access, and foundation engineering requirements add substantial costs. Retaining walls and soil stabilization work further inflate final rebuild estimates.

This explains why premiums are substantially higher for hillside homes. Insurers base coverage on actual rebuild cost, not market value. Understanding this cost reality helps you anticipate necessary coverage levels and premium ranges.

California Home Insurance Context: National Perspective

While Laguna Hills faces unique hillside risks, California homeowners actually benefit from lower average premiums than the national average. According to MoneyGeek’s 2026 research, California’s average homeowners insurance runs approximately $1,543 annually compared to the U.S. average of roughly $3,467.

However, Laguna Hills hillside premiums will exceed these state averages due to specific fire and earth movement risks.

| Region | Avg Annual Premium | Difference from National Avg |

| California | ~$1,543 | -55% |

| National Average | ~$3,467 | — |

Why Hillside Homes Are Being Non-Renewed

Many Laguna Hills homeowners are here because their carrier non-renewed them—this anxiety is real and understandable. Multiple factors drive hillside non-renewals in Orange County. Fire modeling technology has advanced significantly, causing carriers to reassess risk in ways that previously insured homes now fail underwriting. Roof age thresholds (typically 15-20 years) trigger automatic underwriting review, and many older hillside properties get declined.

Increased vegetation mapping via satellite imagery reveals wildfire exposure carriers previously underestimated. Reinsurance costs affecting California carriers have forced strategic pullbacks from hillside ZIP codes. Understanding these industry dynamics helps you navigate what feels like a personal rejection—it’s actually systematic market recalibration.

How Old Harbor Insurance Helps Laguna Hills Homeowners

At Old Harbor Insurance, we start by understanding your hillside property’s specific risks: wildfire exposure, earth movement vulnerability, earthquake risk, and proximity to wildland interface. Then we work our carrier relationships to find coverage that actually fits your situation.

We also help you understand gaps and which mitigation investments can lower premiums. Our job is to make sure you’re protected without overpaying.

Protect Your Hillside Home Today

Your Laguna Hills home is likely your largest financial investment. Protecting it with insurance that covers your actual hillside risks isn’t optional—it’s essential. With the right guidance, you can find adequate coverage at reasonable cost.

Getting started takes just one conversation. Contact Old Harbor Insurance at (951) 297-9740, email info@oldharbor.com, or get a quote online. One of our agents will review your coverage, identify gaps, and build a protection plan that matches your hillside home.

Frequently Asked Questions

What specific risks are unique to hillside homes in Laguna Hills?

Hillside properties face wildfire exposure from proximity to wildland interfaces and earth movement risks including landslides and mudslides. These hazards require specialized coverage evaluation and often trigger higher premiums. Understanding these unique risks helps you anticipate coverage needs and costs.

How does earthquake risk affect my home insurance in Laguna Hills?

Standard homeowners insurance does not cover earthquake damage in California—you must purchase separate earthquake insurance. Given Laguna Hills’ location in a seismically active region, many homeowners opt for at least some earthquake coverage. The cost-benefit analysis depends on your home’s value and deductible tolerance.

What natural hazards aren’t covered by my standard homeowners policy?

Standard policies exclude flood damage, earthquake damage, earth movement (including landslides and mudslides), sinkholes, and long-term maintenance issues. For Laguna Hills hillside properties, these exclusions are critical gaps. Flood and earthquake insurance can be purchased separately.

How can I reduce wildfire risk and lower my insurance costs?

Practical mitigation steps recognized by carriers include creating ember-resistant zones, installing fire-resistant roofing, and managing vegetation on your property. Many carriers offer 5-15% discounts for verified mitigation work. Ask your agent which improvements your specific carrier incentivizes.

Are homes on slopes more expensive to insure than valley properties?

Yes, significantly. Hillside location increases wildfire exposure and earth movement risk, both of which carriers price accordingly. Slopes with vegetation exposure and proximity to wildland interfaces face substantially higher premiums. This is why working with an agent familiar with hillside underwriting matters.

What should I do if I can’t find standard insurance for my Laguna Hills home?

The California FAIR Plan is available as a last resort, providing basic fire coverage when private insurers decline you. However, FAIR Plan coverage is limited and doesn’t include flood, earthquake, or earth movement coverage. Work with an independent agent who can explore all available options.

How often should I review my hillside home insurance policy?

Review your policy annually or whenever you make fire mitigation improvements, complete vegetation management work, or experience major changes. Mitigation improvements that qualify for discounts and changes in home value should trigger policy reviews.