Newport Beach homeowners face risks most of the country doesn’t. Coastal properties here are high-value assets exposed to saltwater corrosion, flooding, wildfire risk, and volatile weather—threats standard homeowners policies often fail to address. Old Harbor Insurance helps local homeowners build coverage designed for coastal realities, not inland templates.

What matters is this: replacement costs are far higher than standard limits, coastal risks need specialized coverage, and the wrong policy can be financially devastating. The right protection lets you enjoy your home with confidence—knowing what you’ve built is truly protected.

Why Standard Homeowners Insurance Falls Short in Newport Beach

Newport Beach’s median home value exceeds $3 million, but here’s the problem: most standard homeowners insurance policies have coverage limits far below that threshold. A $500,000 dwelling coverage limit on a $4 million home leaves you massively underinsured. When a claim happens, that gap between coverage and actual replacement costs becomes a financial catastrophe you can’t recover from.

Beyond replacement cost, Newport Beach homes face coastal hazards that standard policies often exclude. Saltwater corrosion accelerates damage to HVAC systems, roofing, windows, and metal fixtures—up to 3–5 times faster near the coast, according to CAL FIRE and coastal research. Flood damage is also excluded from standard policies, requiring separate flood insurance, and wildfire risk remains a concern during Santa Ana wind events. Standard coverage simply isn’t built for these coastal realities.

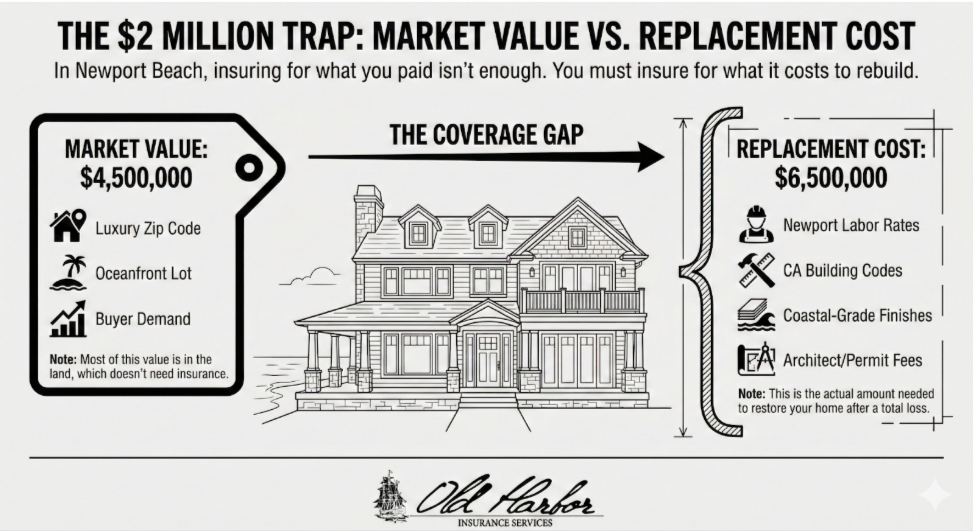

Understanding Coverage Limits: Why Replacement Cost Matters More Than You Think

When you receive a homeowners insurance quote, the first figure you see is the dwelling coverage limit—the maximum your insurer will pay to rebuild your home. This amount must reflect your home’s replacement cost, not its market value, which is a critical distinction in Newport Beach.

A home may sell for $3–5 million due to location and views, but rebuilding it could cost $6+ million once labor, materials, architect fees, and local building standards are factored in. If your policy limits coverage to $2.5 million, you’d be responsible for the remaining shortfall after a total loss—potentially millions out of pocket.

Why Online Replacement Cost Estimates Fall Short for Coastal California Homes

The California Department of Insurance recommends that coastal homeowners work with an insurance professional to conduct a detailed replacement cost analysis rather than relying on quick online estimates. This analysis accounts for local labor rates, California building code requirements, and material costs specific to your area. Old Harbor Insurance conducts these analyses for every Newport Beach client—it’s not optional if you want genuine protection.

Coastal-Specific Risks: Saltwater Corrosion and Your Home’s Systems

Coastal air accelerates corrosion of metal components, causing faster wear to HVAC systems, water heaters, electrical equipment, roofing, gutters, and outdoor fixtures compared to inland homes.

Why insurance won’t cover it

Standard homeowners policies cover sudden damage—but corrosion is considered gradual wear and tear and is excluded. That means failures caused by salt exposure aren’t covered, creating ongoing out-of-pocket costs rather than one-time losses.

What homeowners should do

- Plan for more frequent replacement of exposed systems

- Use coastal-rated materials (stainless steel fixtures, vinyl or plastic gutters)

- Install HVAC systems designed for coastal environments

- Ask your agent about carrier discounts for corrosion-resistant upgrades

Proactive planning and material choices help reduce long-term costs that insurance won’t absorb.

Flood Insurance: The Separate Policy Most Newport Beach Homeowners Don’t Have

Here’s a fact that surprises many Newport Beach homeowners: standard homeowners insurance does not cover flood damage at all. Storm surge, heavy rain flooding, and tsunamis are completely excluded. While lenders usually require flood insurance for mortgaged homes, many homeowners without mortgages skip it—often assuming they’re covered. That misconception can lead to devastating out-of-pocket losses when flooding occurs.

Flood Risk Is Location-Specific, Not Assumption-Based

According to FEMA and the National Flood Insurance Program (NFIP), coastal communities like Newport Beach fall into moderate-to-high flood risk zones depending on exact location. Flood risk is determined using FEMA flood maps—not elevation assumptions or past experience. Some Newport Beach properties are in FEMA flood zones; others aren’t. Don’t assume your property is safe based on intuition or anecdotal evidence.

Flood Insurance Options for Newport Beach Homes

Flood insurance through the National Flood Insurance Program is available for most Newport Beach homes and is often more affordable than expected—sometimes $500–$1,500 annually depending on flood zone. Private flood insurance may offer higher limits or better pricing. Old Harbor Insurance can review your FEMA flood map, assess your risk, and secure the right coverage.

Wildfire Risk and Insurance Availability in California

While Newport Beach is less exposed than inland Orange County, wildfire risk across California is expanding. CAL FIRE reports longer, more intense fire seasons, with fires spreading faster and farther than historical norms.

For homeowners, this has tightened the insurance market. Many carriers now limit new policies or raise rates, and some high-risk properties are pushed into the California FAIR Plan—a last-resort option with limited coverage and higher cost.

How Independent Access Protects Newport Beach Homeowners

As an independent agency with access to 81 carriers, Old Harbor Insurance can place coverage with specialty and regional insurers that still write Newport Beach homes. We also access wildfire mitigation credits and endorsements for properties with defensible space—options typically unavailable through call centers or single-carrier agents.

California’s Homeowners Insurance Regulations: What Newport Beach Residents Should Know

California’s insurance market operates under specific regulatory guidelines that protect homeowners but also create constraints that many people don’t understand. The California Department of Insurance (CDI) oversees all homeowners policies issued in the state and enforces consumer protections that some other states don’t offer.

What These Protections Mean for Newport Beach Homeowners

Under California Insurance Code § 1861.05, insurers cannot cancel or non-renew a policy solely due to a home’s age or roof condition. Policies must also include baseline coverages—such as debris removal, ordinance or law compliance, and replacement-cost personal property—that many other states allow insurers to restrict. Understanding these protections helps homeowners recognize inadequate policies and know when independent review is essential.

How Old Harbor Insurance Helps Newport Beach Homeowners Build Proper Coastal Coverage

Old Harbor Insurance takes a coastal-specific approach to homeowners coverage. We understand Newport Beach risks, California insurance regulations, and the realities of insuring high-value coastal homes—unlike national carriers that apply inland templates to coastal properties.

Our process is straightforward and thorough:

- Accurate replacement cost analysis: We calculate true rebuild costs using Newport Beach labor rates, local building codes, and material pricing.

- Coastal risk assessment: We evaluate flood zone status, saltwater corrosion exposure, wildfire proximity, and storm-surge risk.

Coverage gap review: We identify exclusions or limits in your current policy and recommend targeted endorsements or supplemental coverage. - Independent carrier matching: With access to 81 partner carriers, we place coverage based on fit—not quotas—so you get the best balance of protection, pricing, and service.

The result is coverage built for your property’s actual risks, backed by carriers willing to insure Newport Beach homes properly.

Protect Your Coastal Investment Today

Your Newport Beach home is likely your most valuable asset and irreplaceable in many ways. Standard insurance doesn’t cut it. You need coverage designed for coastal reality, not mainland assumptions. You need an agent who understands your specific risks and has access to carriers willing to properly insure high-value coastal properties.

Old Harbor Insurance is ready to review your coverage and ensure you’re genuinely protected. Call us at (951) 297-9740, email info@oldharbor.com, or fill out a quick quote form on our website. One of our licensed agents will contact you within 24 hours to discuss your Newport Beach property and build coverage that actually matches your coastal exposure and asset value. Your protection is just one conversation away.

Frequently Asked Questions

How much homeowners insurance coverage do I actually need in Newport Beach?

Your dwelling coverage should reflect your home’s actual replacement cost in today’s market with Newport Beach labor and materials factored in. This is typically higher than your home’s market value. We recommend a detailed replacement cost analysis rather than guessing. Most Newport Beach homes need $2-5 million in dwelling coverage depending on size and location.

Does my homeowners policy cover flood damage?

No. Standard homeowners insurance explicitly excludes flood damage. You need a separate flood insurance policy if your property is in a flood zone or at flood risk. Even if your property isn’t in an official FEMA flood zone, flood damage from heavy rain or storm surge isn’t covered by homeowners insurance.

What’s the difference between NFIP flood insurance and private flood insurance?

The National Flood Insurance Program (NFIP) is government-backed and available for most properties. Private flood insurance is offered by commercial insurers and sometimes offers better rates, higher coverage limits, or faster claims processing. An independent agent can compare both options for your specific property.

Does my homeowners policy cover saltwater corrosion damage?

No. Corrosion is considered gradual wear and tear, which is excluded from standard policies. However, sudden damage to corroded components might be covered. The best approach is maintenance and material upgrades—stainless steel fixtures, coastal-rated HVAC systems, and protective coatings reduce corrosion damage.

What’s the California FAIR Plan and when would I need it?

The California FAIR Plan is a state-run insurer of last resort. If standard carriers decline your property due to fire risk or other factors, you can get basic coverage through the FAIR Plan. However, FAIR Plan coverage is minimal and expensive. As an independent agent, we work hard to find you better options before FAIR Plan becomes necessary.

Can an insurance company cancel my homeowners policy in California?

Not easily. California law protects homeowners from cancellation or non-renewal based solely on property age or roof age. Insurers must have specific, documented reasons for cancellation—and you have rights to appeal. If your carrier threatens cancellation, contact the California Department of Insurance or speak with an independent agent about your options.

How often should I review my homeowners insurance coverage?

We recommend annual reviews, especially in Newport Beach where property values fluctuate and coastal risks evolve. At minimum, review coverage when you make home improvements, after major storms or fire seasons, or if nearby properties experience losses. Your coverage should increase as your home’s replacement cost increases.