Living in La Jolla offers stunning coastline—but also insurance risks national carriers often miss. Salt corrosion, coastal erosion, wildfire exposure, and flood risk can leave gaps in standard policies. Old Harbor Insurance helps La Jolla homeowners secure coverage built for coastal living.

What may surprise you is that the right coastal coverage often costs less than expected when you work with an independent agent who can compare multiple carriers. Keep reading to see what your La Jolla home truly needs—and where your current policy may be falling short.

Understanding Coastal Property Risks in La Jolla

La Jolla isn’t just beautiful—it’s exposed to environmental forces many homeowners underestimate. According to U.S. Geological Survey coastal assessments, Southern California shorelines erode an average of 2–4 inches per year, with heavier losses during severe storm seasons. Salt air, constant moisture, and coastal construction demands create insurance and maintenance challenges that differ sharply from inland San Diego homes.

Flood Risk Beyond the Beachfront

Federal Emergency Management Agency flood maps show many La Jolla neighborhoods fall within high-risk flood zones—even when they’re not directly on the water. Standard homeowners insurance does not cover flood damage, leaving many properties exposed to catastrophic loss without a separate flood policy.

Wildfire & Compounding Coastal Risks

Beyond erosion and flooding, La Jolla also faces wildfire exposure during extreme Santa Ana wind events. CAL FIRE hazard maps place some coastal San Diego areas in moderate to high fire severity zones, depending on location and vegetation. When combined—erosion, flood risk, wildfire exposure, and weather damage—these factors create a complex insurance puzzle that requires specialized coastal expertise to solve correctly.

The Carrier Non-Renewal Crisis Hitting San Diego

San Diego County—including La Jolla—is facing a growing insurance carrier withdrawal. Major insurers are non-renewing large numbers of coastal policies, leaving thousands of homeowners without traditional coverage options. This isn’t an isolated neighborhood issue; it’s a systemic disruption across California’s coastal insurance market, with San Diego among the hardest hit regions.

Why Non-Renewals Are Accelerating

The California Department of Insurance tracks residential non-renewals and FAIR Plan growth to monitor availability risks. As carriers exit coastal markets, many homeowners are pushed into the California FAIR Plan—a last-resort option that is costly, limited in scope, and poorly suited for high-value coastal homes.

Common consequences of carrier exits include:

- Forced placement into FAIR Plan coverage

- Higher premiums with reduced protection

- No customization for coastal-specific risks

- Increased exposure to uncovered losses

Why an Independent Agent Matters

This market shift is exactly why working with Old Harbor Insurance is critical. As an independent agency, we maintain active relationships with carriers still writing coastal coverage—providing alternatives when national insurers pull back and helping La Jolla homeowners avoid being trapped in last-resort policies.

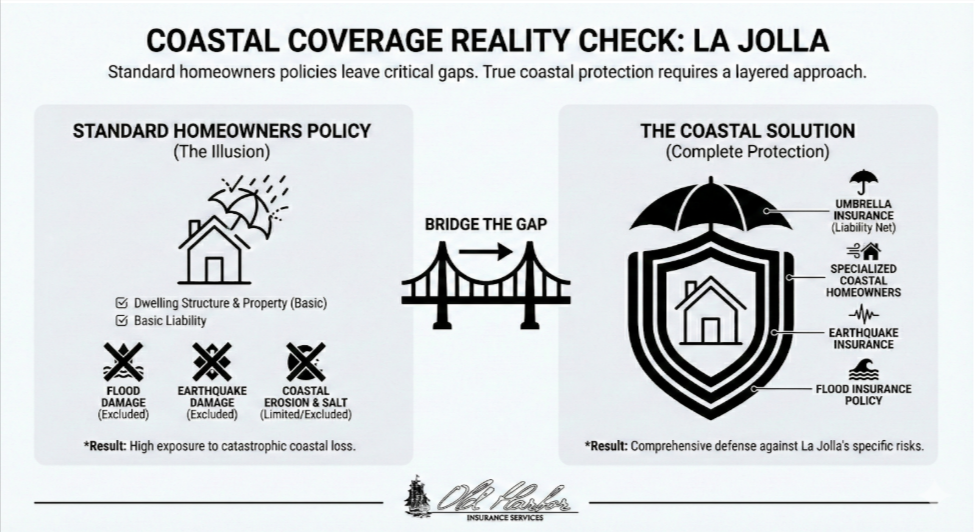

Standard Homeowners Policy Gaps at the Coast

Most homeowners policies are built for inland, suburban homes—not coastal properties. They often exclude flood and earthquake damage and underestimate risks like erosion and salt-air deterioration. For La Jolla homeowners, this can mean having coverage that looks adequate on paper but fails during a coastal storm or non-renewal.

As carriers increasingly exit coastal markets, these gaps have become impossible to ignore. A policy that doesn’t address flood, earthquake, and wildfire risk is incomplete for coastal California homes. Old Harbor Insurance helps homeowners see what their policy truly covers—and where protection is missing.

Coastal Flood Insurance: Non-Negotiable for La Jolla

Flood damage is the costliest risk in La Jolla, yet it’s completely excluded from standard homeowners insurance. Flood coverage is available through the National Flood Insurance Program or private insurers. If your home sits in a FEMA-designated high-risk zone, lenders require flood insurance—but even outside those zones, going without it exposes you to catastrophic loss.

How Flood Zones Affect Coverage & Cost

Federal Emergency Management Agency Flood Insurance Rate Maps determine your property’s risk level, premiums, and coverage requirements. While high-risk zones carry higher premiums, being uninsured is far more costly. Old Harbor Insurance helps La Jolla homeowners assess their flood risk and compare NFIP and private options to secure the right limits at competitive rates.

Earthquake Insurance: Critical for Coastal Seismic Risk

Living on Southern California’s coast means living with earthquake risk. While earthquake damage is catastrophic, it’s also entirely excluded from standard homeowners policies and California FAIR Plan coverage. According to the U.S. Geological Survey’s earthquake probability assessments for California, the San Diego region faces a significant earthquake probability over the next 30 years, making earthquake insurance critically important for coastal properties.

Earthquake policies are available through California’s Earthquake Authority and private carriers, typically offering 15% of your home’s replacement cost in coverage with a 25% deductible. For a $2 million home in La Jolla, that means $300,000 in protection without catastrophic out-of-pocket exposure if a major earthquake strikes.

Wildfire Risk: Why La Jolla Coastal Properties Are Exposed

Even though La Jolla isn’t a high-density fire zone, wildfire risk remains—especially during Santa Ana wind events. CAL FIRE maps show that even moderate fire hazard zones trigger added insurer scrutiny, directly affecting renewals.

As wildfire and weather risks combine, carriers are becoming more selective with coastal policies, according to the California Department of Insurance. Even moderate fire exposure can impact your ability to keep coverage. Old Harbor Insurance works with carriers that price wildfire risk realistically—without abandoning coastal homeowners.

Umbrella Insurance for Coastal Liability Exposure

Coastal homes in La Jolla attract more foot traffic from beach access, scenic views, and neighborhood walks—raising liability risk compared to inland properties. According to the Insurance Information Institute, liability claims tend to be higher in coastal areas due to increased visitors and activity.

Umbrella insurance extends your homeowners liability limits and protects your assets. For La Jolla homeowners, $1–2 million in coverage is commonly recommended and typically costs only a few hundred dollars per year—delivering significant protection at a relatively low cost.

How Old Harbor Insurance Helps La Jolla Homeowners

Old Harbor Insurance combines local coastal expertise with access to 81 insurance carriers—something national insurers can’t offer. We work with La Jolla homeowners daily, assessing property-specific risks and building coverage strategies that actually fit coastal living.

What sets us apart:

- Local knowledge of La Jolla’s coastal risks

- Access to specialty and admitted carriers

- Solutions for carrier non-renewals and premium spikes

- Competitive options unavailable through direct national carriers

Your Local Partner in a Non-Renewal Market

As insurers exit coastal markets, we focus on carriers still writing coastal coverage—helping homeowners avoid last-resort policies. Whether you’ve been non-renewed, hit with higher premiums, or want a second opinion, we find workable solutions when others can’t.

Your Peace of Mind Starts Here

The right mix of flood, earthquake, and umbrella coverage protects your home against real coastal risks. Old Harbor Insurance has helped hundreds of San Diego County homeowners move from uncertainty to confidence.

Call: (951) 297-9740

Email: info@oldharbor.com

Free quote online — a licensed agent will review your coverage within 24 hours.

Frequently Asked Questions

What does homeowners insurance actually cover at the coast?

Standard homeowners insurance covers dwelling structure, personal property, liability, and living expenses if your home is uninhabitable. However, it specifically excludes flood, earthquake, and often provides limited coverage for salt spray damage or coastal erosion. That’s why coastal homeowners need additional policies to fill these gaps.

Will my mortgage lender require flood insurance?

Yes—if your property is in a FEMA-designated high-risk flood zone (Zone A or AE), your mortgage lender will require flood insurance as a condition of the loan. Even if you’re not in a high-risk zone, we recommend it for La Jolla properties given coastal exposure and the actual frequency of local flooding.

Why are carriers non-renewing coastal policies in San Diego?

Carriers nationwide are exiting coastal markets due to increased claims frequency, rising repair costs, and catastrophic wildfire losses. San Diego County has been particularly affected, with major carriers dropping tens of thousands of policies. This has created unprecedented market pressure, but Old Harbor Insurance maintains relationships with carriers still actively writing coverage in Southern California coastal areas.

How much earthquake coverage should I get?

Most insurance experts recommend purchasing the maximum coverage available. California Earthquake Authority policies offer 15% of dwelling coverage with a 25% deductible. For a $2 million home, that’s $300,000 in coverage—expensive, but far less than rebuilding after a major earthquake.

Can I get flood insurance if I don’t have it now?

Yes—flood policies are always available, though there’s a 30-day waiting period for standard NFIP policies (14 days for private insurers). If you’re concerned about coastal risk, applying immediately protects you from sudden premium increases or coverage gaps.

What’s the difference between FAIR Plan and regular homeowners insurance?

FAIR Plan is a coverage of last resort for homeowners who can’t obtain insurance through standard markets. It’s typically more expensive, offers less comprehensive coverage, and includes higher deductibles. We help homeowners avoid FAIR Plan by finding superior alternative coverage at competitive rates.

How often should I review my coastal coverage?

We recommend reviewing your coastal coverage annually—at minimum when you renew. Market conditions change rapidly, carrier availability shifts, and your property’s exposure may have increased due to neighborhood development or coastal erosion. Annual reviews ensure your coverage stays current with your actual needs.