Anaheim homeowners face an insurance landscape unlike coastal or rural areas, with wildfire exposure during Santa Ana season, aging 1960s–1980s housing stock, and a tightening market. Many don’t realize their coverage is outdated until a claim or non-renewal. Old Harbor Insurance helps build coverage tailored to neighborhood risks and current conditions.

The average Anaheim home is underinsured by 20–30%, while premiums rise as carriers reassess Orange County risk. Knowing what you need—and securing it before the market tightens further—is essential.

Anaheim’s Specific Insurance Landscape

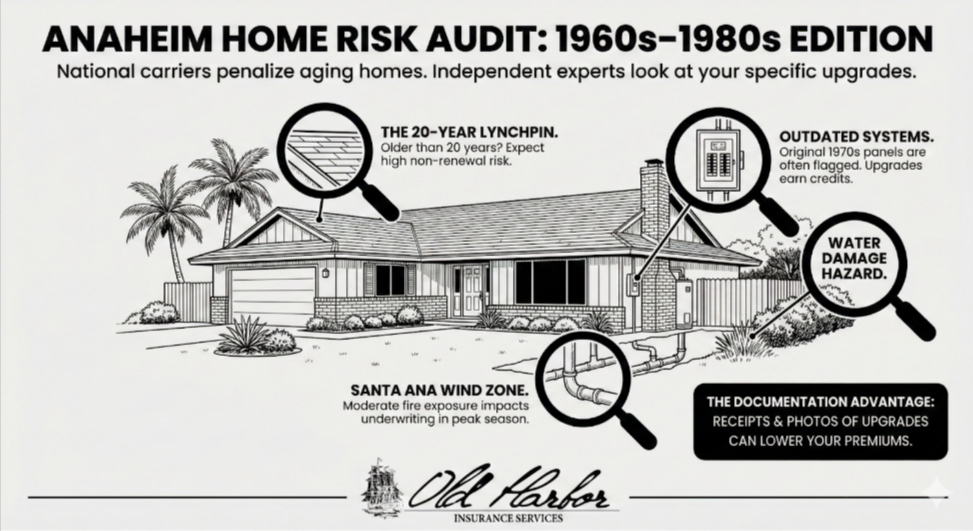

Anaheim isn’t coastal, but many neighborhoods were built in the 1960s–1980s, bringing higher insurance risk from aging roofs, outdated electrical systems, and older plumbing. As homes age, carriers increasingly respond with higher premiums or non-renewals due to elevated loss exposure.

Wildfire Exposure During Santa Ana Season

While Anaheim isn’t a high-density mountain fire zone, California Department of Insurance wildfire risk data shows that even moderate fire exposure affects underwriting—especially during Santa Ana wind events. Risk varies by neighborhood based on vegetation and proximity to wildland areas.

A Tightening Statewide Insurance Market

Across California, insurers are raising rates, tightening guidelines, and selectively non-renewing properties they view as marginal risks. In this environment, securing affordable coverage depends on knowing which carriers still actively value Anaheim properties and how to position your home correctly.

How Home Insurance Pricing Works in California

Understanding premium calculation helps you see why local expertise matters. According to the California Department of Insurance, homeowners insurance premiums are regulated by state law and vary based on fire protection ratings, building age, construction type, coverage limits, and deductible choices. All carriers must file rates for CDI approval before implementation.

Different carriers apply different underwriting criteria to Anaheim properties. One carrier might penalize your 1970s home heavily, while another views well-maintained older homes more favorably. A local independent agent knows which carriers’ underwriting aligns with your specific property’s profile.

Home Age and Condition: The Documentation Advantage

Insurance carriers don’t treat a 1970s Anaheim home the same as new construction—older homes do present different risks. However, they often apply blanket penalties without examining your specific home’s condition. If your roof was replaced in 2019, electrical system upgraded in 2015, and plumbing updated in 2018, your home is far less risky than similar-age homes with original systems—yet many insurers charge the same premium.

Presenting your home’s actual condition matters enormously. Documentation of roof age, electrical updates, plumbing renovations, and HVAC replacements directly impacts carrier decisions and premium rates. Understanding how your specific improvements affect carrier perception helps Old Harbor Insurance negotiate better rates and find carriers who value updated properties.

The Roof Question: Orange County’s Insurance Lynchpin

Roof age is often the single most important factor affecting insurability and premiums in Orange County. Most carriers follow strict guidelines:

- Over 20 years: High risk of non-renewal or sharp premium increases

- 15–20 years: Enhanced scrutiny and higher rates

- Newer roofs: Access to more carriers and better pricing

Even a well-maintained roof over 20 years old can limit options, while a newer roof opens doors to competitive coverage. For many Anaheim homes, a $12,000–$15,000 roof replacement pays for itself within 3–5 years through lower premiums. Knowing your roof’s true age and condition—not county estimates—is essential before shopping for insurance.

Water Damage Risk in Older Homes

Anaheim’s aging housing stock carries elevated water damage risk compared to newer neighborhoods. Older plumbing systems fail more often, foundations may allow water intrusion during heavy rains, and aging roofs can develop slow leaks that go unnoticed for months.

Insurers closely track prior water damage claims. Even a single pipe burst years ago can affect eligibility or pricing. If you’ve had past losses, showing mitigation—such as repipes, plumbing inspections, water detection systems, or gutter maintenance—helps secure acceptable underwriting terms.

Replacement Cost vs. Actual Cash Value

Many homeowners choose low-cost policies without understanding a crucial difference.

- Actual Cash Value (ACV): Pays depreciated value

- Replacement Cost: Pays the full cost to rebuild

On an $800,000 Anaheim home, an ACV policy might reimburse only $600,000 after depreciation—leaving a $200,000 gap. Ensuring your policy includes replacement cost coverage at proper limits is fundamental to real financial protection.

Anaheim Hazard Profile: Flood, Fire, and Climate Trends

While Anaheim isn’t coastal or a high-fire mountain area, properties still face real hazards. Some neighborhoods have moderate flood risk near the Santa Ana River flood plains, and fire exposure varies based on proximity to wildland areas.

Climate shifts across Orange County are changing risk profiles—drought increases fire danger, while atmospheric rivers bring flash flood threats. Coverage that was adequate years ago may no longer be enough. Understanding your property’s specific risks—not citywide averages—helps determine whether you need added protection beyond standard policies.

Neighborhood Risk Variation

Anaheim isn’t monolithic for insurance purposes. Some neighborhoods present lower risk than older, more isolated areas. Some have higher burglary rates, affecting liability and personal property coverage needs. Some have been hit by multiple fire-related claims, making carriers more selective.

Understanding your specific neighborhood’s insurance history helps Old Harbor Insurance find carriers most willing to insure properties like yours. We assess block-by-block risk factors affecting your property’s insurability and cost.

Personal Liability and Umbrella Coverage

Liability coverage protects you if someone is injured on your property or if you damage someone else’s property—claims that happen more often than homeowners expect. A slip-and-fall lawsuit or storm damage to a neighbor’s car can quickly become costly, making liability coverage your financial shield.

Most policies include $300,000 in liability coverage, which can fall short in a serious injury claim. In denser areas like Anaheim, higher foot traffic increases exposure. Umbrella insurance adds $1–2 million in protection for just a few hundred dollars per year, safeguarding your assets beyond standard limits.

What Happens When Private Coverage Isn’t Available?

As California’s insurance market tightens, some homeowners face rejection or non-renewal from traditional carriers. When private coverage becomes unavailable, California’s FAIR Plan provides a coverage of last resort—a state-regulated program ensuring homeowners can obtain basic fire and property coverage when private insurers won’t.

FAIR Plan policies have major limitations, often excluding liability, water damage, and other common perils while carrying higher premiums and restrictive limits. They’re meant as a last-resort safety net—not a long-term solution—making proactive planning with a local independent agent essential to avoid them.

The Independent Agent Advantage

The Orange County insurance market is tightening as carriers raise rates and limit new business. For Anaheim homeowners, relying on a single national carrier is risky—working with an independent agent who has access to multiple and specialty markets is key to securing fair, adequate coverage.

Old Harbor Insurance partners with carriers still valuing Anaheim properties. We understand the current market pulse, which carriers have tight guidelines, and which remain competitive. We know how to present your property’s advantages to get the best possible rates and underwriting terms.

Preparing Your Anaheim Home for Natural Disasters

Comprehensive insurance is only part of disaster preparedness. The City of Anaheim’s Hazard Mitigation Plan emphasizes that residents should include insurance coverage as a critical component of overall disaster readiness. Beyond policy coverage, preparing your home includes physical hardening—securing loose items, maintaining gutters, trimming vegetation from your roof, and ensuring your water heater is strapped.

Your insurance strategy should align with physical preparedness efforts. If you’ve hardened your home against wind damage, invested in fire-resistant landscaping, or installed a water detection system, your insurance agent should know because these improvements may qualify you for discounts or better underwriting terms.

Your Insurance Foundation Starts Today

Insurance pressure on Anaheim homeowners continues to rise—and waiting only limits your options. Roof age, home condition documentation, neighborhood risk factors, and carrier availability all directly affect your coverage and costs. Reviewing your policy now, understanding what’s actually covered, and confirming replacement cost protection are essential steps.

How Old Harbor Insurance Helps

Old Harbor Insurance builds strategies matched to your home’s specific risk profile and financial goals. Whether you’ve been non-renewed, hit with premium increases, or simply want a second opinion, we identify solutions that work in today’s market.

(951) 297-9740

info@oldharbor.com

Get a quote online

We’ll review your home’s condition, evaluate your current coverage, and find opportunities to improve protection while managing costs.

Frequently Asked Questions

Why do insurers care so much about roof age?

Roof age is a primary driver of claim frequency and severity. Older roofs fail during storms, leak during heavy rain, and require replacement. Carriers view roof age as a direct indicator of property condition and maintenance. A 20+ year old roof signals higher risk regardless of other factors.

Should I get a roof inspection before shopping for insurance?

Yes. A professional roof inspection documenting actual condition costs $200-$400 and could save thousands in premiums by proving your roof is in better condition than its age suggests. Providing inspection documentation shows carriers you maintain your property.

What’s the difference between HO-3 and HO-5 homeowners policies?

HO-3 is the standard policy covering your home and personal property on a “named perils” basis—only damage from specified causes is covered. HO-5 is broader, covering losses on a more comprehensive basis with fewer exclusions. HO-5 costs more but provides better protection, especially for older homes.

Do I need earthquake insurance in Orange County?

Southern California faces seismic risk, and earthquake damage is completely excluded from standard homeowners policies. Whether you purchase it depends on your risk tolerance and financial ability. For older homes, earthquake damage could exceed $100,000, making coverage worth considering.

What should I document about my home’s condition?

Photograph and document the age of major systems: roof installation date, electrical panel upgrade date, plumbing replacement date, HVAC system age, foundation condition, and any renovations. Keep receipts for major work. This documentation helps negotiate better rates.

How often should I review my Anaheim homeowners policy?

We recommend annual reviews, especially if you’ve made significant improvements or the insurance market shifts (which it does frequently in Orange County). Even small changes—new roof, electrical upgrades, or security systems—can qualify you for better rates with different carriers.

What’s happening to the Orange County insurance market right now?

Carriers are reevaluating risk across Orange County, tightening underwriting, raising rates, and sometimes non-renewing marginal risks. Understanding your carrier’s financial health and willingness to write Anaheim properties is more important than ever. This is why an independent agent monitoring market trends is invaluable.