Santa Ana homeowners face insurance challenges tied to seismic risk, wildfire exposure, and rising construction costs. Generic national policies often miss local realities, while working with an independent agent can deliver better protection and real savings. Old Harbor Insurance understands Santa Ana’s market in ways national carriers can’t.

Insurance costs vary widely by ZIP code and risk factors. Knowing what drives your premium—and how to position your home with the right carrier—can mean the difference between overpaying and securing competitive rates.

Understanding Santa Ana’s Insurance Market Landscape

Santa Ana operates within Orange County’s insurance market but has its own pricing dynamics. In 2025, California’s homeowners market continues to see rate increases and carrier consolidation. Premiums can vary widely by ZIP code—some areas see lower rates, while others face higher costs due to localized risk and claim history.

How Your Address Affects Your Premium

Your exact address plays a major role in pricing. Carriers evaluate seismic risk first, then wildfire zones, flood exposure, home age, and construction type. Understanding how insurers score these factors allows Old Harbor Insurance to match Santa Ana homes with carriers offering the most competitive terms.

When private coverage becomes difficult to obtain in high-risk areas, homeowners may turn to California’s FAIR Plan—a coverage of last resort that’s typically 30-50% more expensive and provides more limited protection than standard policies. Avoiding the FAIR Plan through proactive insurance planning with an independent agent who understands the current market is precisely why local expertise matters right now.

Local Risk Factors Affecting Your Premium

Seismic activity is the primary natural disaster threat affecting Santa Ana homeowners. According to the U.S. Geological Survey’s earthquake probability assessments for California, the Santa Ana region faces significant seismic risk. Standard homeowners policies completely exclude earthquake damage, yet this makes earthquake insurance a critical consideration for comprehensive protection—something national carriers often downplay when you’re shopping online.

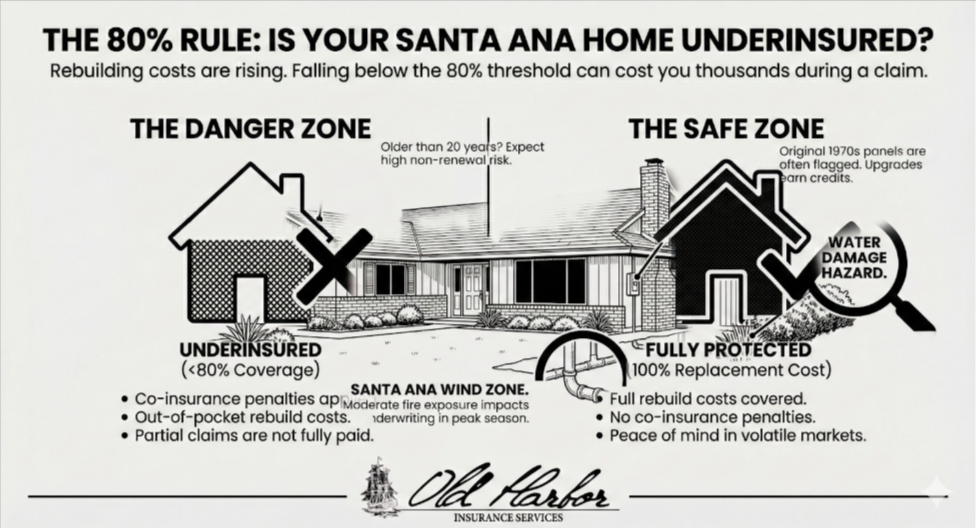

Wildfire, Flood, and the 80% Rule

Wildfire risk still affects Santa Ana insurance costs. While not a high-density fire zone, moderate exposure from nearby vegetation and wildland areas is closely evaluated by carriers, as shown in CAL FIRE hazard maps. Flood and mudslide risk during heavy rains adds further neighborhood-specific exposure.

The industry’s “80% rule” also matters. Insurers typically require dwelling coverage at least 80% of replacement value to pay full rebuild costs. With rising construction prices, many Santa Ana homes that were adequately insured years ago may now be underinsured, making accurate replacement cost calculations critical.

Essential Homeowners Insurance Coverage

Standard homeowners insurance includes three main components: dwelling coverage (your home’s structure), personal property coverage (your belongings), and liability coverage (protection if someone is injured on your property).

For Santa Ana homeowners in 2025, rebuilding costs range significantly depending on neighborhood, home age, and square footage. A typical Santa Ana home valued at $600,000-$800,000 requires dwelling coverage matching those replacement costs—not market value.

Personal Property, Liability, and 2025 Enhancements

Personal property coverage protects your belongings, which many Santa Ana homeowners underestimate in value. Liability coverage usually starts at $300,000 and is especially important in denser neighborhoods where foot traffic—and exposure—is higher.

California’s 2025 regulations also strengthen protection. Insurers must include at least 10% code upgrade coverage, and additional living expense coverage now extends up to 36 months during declared emergencies, giving displaced homeowners more time to recover.

Additional Coverage Santa Ana Homeowners Should Consider

Earthquake insurance is critical for Santa Ana residents. The California Earthquake Authority (CEA) offers earthquake coverage specifically designed for California homeowners. Since standard policies exclude earthquake damage entirely, and earthquake damage could easily exceed $100,000 for significant events, separate earthquake coverage should be a priority consideration based on your financial situation and risk tolerance.

Flood Insurance and Home Hardening

Flood damage isn’t covered by standard policies, so separate flood insurance may be necessary based on FEMA flood maps and neighborhood history. Adding umbrella liability coverage of $1–2 million costs only a few hundred dollars annually and protects assets beyond basic limits.

Home hardening—upgraded roofing, defensible space, and fire-resistant features—can significantly reduce premiums. Meeting newer California building code standards may also qualify your home for insurance discounts.

How Independent Agents Add Real Value

Working with an independent agent like Old Harbor Insurance offers benefits online quotes can’t match. Independent agents compare multiple carriers to find coverage that fits your specific needs—not generic packages—and understand Santa Ana–specific risks that algorithms often miss, such as neighborhood fire history, local claim patterns, and common construction issues.

We also maintain relationships with carriers still actively writing Santa Ana properties, unlocking options you won’t see through direct online shopping. Beyond placement, we provide ongoing policy management and hands-on claims support—so when something goes wrong, you have a real advocate who knows your coverage and protects your interests.

Tips for Reducing Your Santa Ana Homeowners Insurance Costs

Deductible selection directly impacts your annual premium. Choosing a higher deductible ($2,500 or $5,000 instead of $1,000) lowers your monthly costs substantially, but only if you can actually afford that out-of-pocket expense during a claim. Bundling homeowners and auto policies with the same carrier typically saves 10-25% on combined premiums.

Claims History, Discounts, and Annual Reviews

A clean claims history matters—many insurers offer discounts after 3–5 claim-free years. Additional savings may come from security systems, fire-resistant upgrades, safer roof construction, and even a strong credit profile, which most carriers factor into pricing.

Annual policy reviews help ensure you’re not missing discounts or underinsured. If you’ve upgraded your home or its value has risen—common in Santa Ana—updating limits to current replacement costs protects you and can unlock better rates with carriers that reward accurately valued homes.

Navigating Claims and Coverage in Santa Ana

California’s 2025 improvements to the claims process provide important protections for homeowners. Insurers must now provide advance payments of 60% of the estimated claim amount, up to $350,000—significantly better than the old 30% requirement. These advance payments help you begin repairs and recovery while the full claim is being processed.

Documentation, Timelines, and Your Rights

Extended claim collection periods now allow 36 months post-emergency to submit proof and receive payment, versus the shorter timelines that previously pressured homeowners. You also have the right to designate your own primary adjuster if you’re unhappy with the insurer’s choice. During declared emergencies, California law provides grace periods that protect your coverage even if you can’t pay your premium immediately.

Understanding your documentation requirements and claim timelines prevents frustrating delays. Keeping detailed records of your home’s condition, contents, and improvements helps when you need to file a claim or demonstrate why your coverage limits need to be higher.

Your Peace of Mind Starts with Local Expertise

Santa Ana homeowners need coverage tailored to neighborhood risks and financial goals. The right mix of dwelling, personal property, liability, earthquake, and flood coverage protects against real exposures, and Old Harbor Insurance helps homeowners move from uncertainty to confidence—whether you’re buying for the first time, facing non-renewal or higher premiums, or seeking a second opinion.

Call us at (951) 297-9740, email info@oldharbor.com, or get a quote online. One of our licensed agents will contact you within 24 hours to assess your home’s specific risks, review your current coverage, and identify opportunities to improve protection while managing costs. Your Santa Ana home’s insurance foundation is worth getting right.

Frequently Asked Questions

What’s the average cost of homeowners insurance in Santa Ana in 2025?

The average Santa Ana homeowner pays approximately $111-$115 per month ($1,332-$1,380 annually) for standard coverage, though this varies significantly by ZIP code, home value, and specific risks. Homes in higher-risk areas or those requiring FAIR Plan coverage pay substantially more.

Why is earthquake insurance important for Santa Ana homeowners?

Santa Ana faces significant seismic activity, and standard homeowners policies do not cover earthquake damage. Separate earthquake coverage is essential for comprehensive protection if you want to guard against this major financial exposure.

What is the 80% rule, and does it apply to Santa Ana?

The 80% rule is an industry standard where insurers provide full replacement cost if your dwelling coverage is at least 80% of your home’s true replacement value. Most Santa Ana insurers require compliance to avoid coverage penalties.

Can I get homeowners insurance if I’m in a wildfire-prone area?

Yes, though options may be limited in high-risk zones. If rejected by private insurers, California’s FAIR Plan serves as an insurer of last resort, though premiums are typically 30-50% higher than private market rates.

How often should I review my Santa Ana homeowners policy?

At least annually, or after major renovations, significant property improvements, or substantial changes in your home’s value. Santa Ana property values have risen dramatically, potentially leaving older policies significantly underinsured.

What new protections did California add to homeowners policies in 2025?

California expanded replacement cost collection periods to 36 months post-emergency, increased advance payments to 60% up to $350,000, and added minimum code upgrade coverage of 10% of dwelling limits.

Why work with an independent agent instead of using online quotes?

Independent agents access multiple carriers, understand local risks that generic algorithms miss, help customize coverage for your specific needs, and provide ongoing support during claims and policy management.

What discounts are typically available for Santa Ana homeowners?

Common discounts include bundling policies, home security systems, claims-free history (3-5 years), fire-resistant upgrades, safe roof construction materials, and loyalty discounts for long-term customers.