Fullerton homeowners face a tightening insurance market shaped by California’s natural hazards and rising replacement costs. Many residents discover their coverage is inadequate, expensive, or unavailable through standard carriers. Old Harbor Insurance works with Fullerton residents to find protection that fits their home and risks.

In this guide, we’ll walk you through what home insurance covers in California, what specific risks threaten Fullerton properties, and why a local independent agent beats going it alone. You’ll understand the threats, your coverage options, and how to protect your investment.

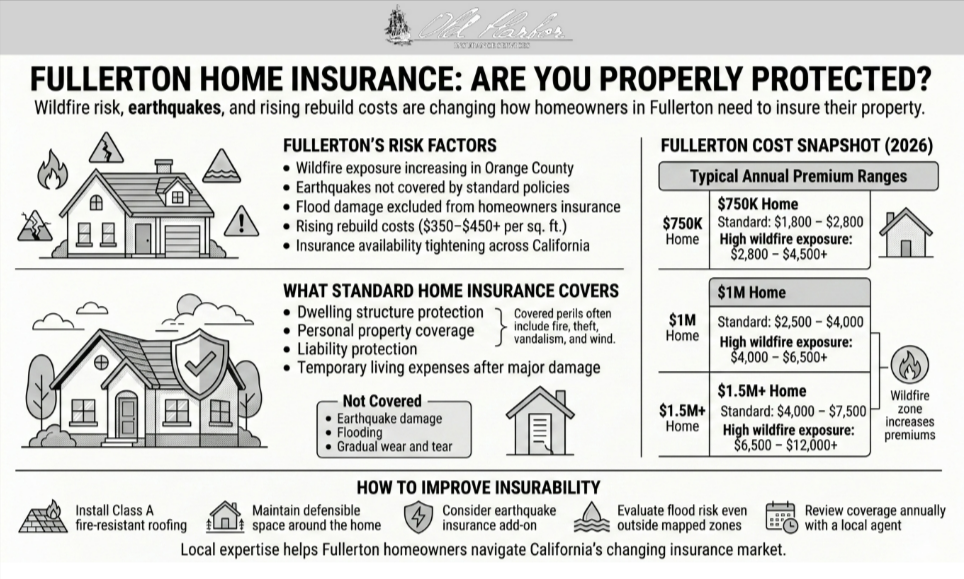

The Fullerton Home Insurance Challenge

Fullerton sits in Orange County facing multiple insurance risks: wildfire exposure, earthquake activity, potential flood exposure, and a tightening carrier market. Recent Fire Hazard Severity Zone updates show expanded Very High Fire Hazard areas in and around Fullerton, making wildfire risk an increasingly relevant factor for homeowners and insurers.

According to the U.S. Department of the Treasury, homeowners insurance premiums have risen significantly above inflation, with availability declining as climate-related risks strain the market. Fullerton residents experience these national trends through higher costs and fewer carrier options.

Understanding Fullerton’s Specific Risks

Fullerton’s Local Hazard Mitigation Plan identifies earthquakes, wildfires, and severe weather as significant property threats. Understanding these local risks explains why certain coverage types matter more for Fullerton homeowners than residents in other regions.

The California Office of the State Fire Marshal maintains official Fire Hazard Severity Zones that classify areas into wildfire risk levels. Knowing your zone helps you understand how carriers assess your property and what coverage options are available to you.

Wildfire Risk: The Insurance Market Driver

Wildfire risk has become the primary factor shaping insurance availability and pricing across Orange County. The California Department of Insurance tracks wildfire losses through biennial reports that show insurers actively tracking fire exposure. This data directly influences underwriting decisions and the rates you’re offered.

The good news? There are concrete steps you can take to reduce wildfire risk and improve your insurance situation. The California Department of Insurance’s Safer from Wildfires program outlines mitigation strategies: Class A fire-resistant roofs, cleared defensible space, ember-resistant zones, and home hardening measures. These improvements may help you qualify for coverage or lower premiums.

Earthquake Coverage: Protection Beyond Standard Policies

Earthquakes aren’t covered by standard homeowners insurance in California, and for Fullerton residents in a seismically active region, this is a critical gap. Earthquake insurance covers structural damage caused by seismic events but comes with deductibles typically 15-20% of your coverage limit—much higher than standard homeowners deductibles.

This decision deserves professional guidance because earthquake risk is real in Fullerton, but the cost must be weighed against your financial capacity to handle potential uninsured damage. Many homeowners find that some level of earthquake coverage makes sense.

Flood Insurance: Why It’s Not Optional in Fullerton

Standard homeowners insurance does not cover flood damage—this is one of the most critical coverage gaps. According to the National Flood Insurance Program, even a few inches of water inside your home can cause tens of thousands of dollars in damage. Flood insurance is the only way to protect against this risk.

If you’re outside a mapped flood zone, flood insurance is optional—but that’s when many homeowners skip it. Flood risk in Fullerton comes from multiple sources including street flooding, stormwater accumulation, and heavy rain events. Having an agent review your specific flood risk is essential.

Understanding What Your Homeowners Policy Actually Covers

The California Department of Insurance’s Residential Property Insurance Report provides statewide data on policy types, coverage amounts, and premiums. Your policy covers your dwelling structure, personal property, liability, and additional living expenses if you relocate temporarily.

Your policy covers sudden, accidental damage from covered perils like fire, theft, vandalism, and wind. But it doesn’t cover earthquake, flood, wear-and-tear, or gradual damage. Understanding these exclusions helps you identify where supplemental coverage might be necessary.

2026 Fullerton Home Insurance Cost Snapshot

Home insurance pricing in Fullerton varies significantly based on wildfire zone classification, home age, construction type, and coverage structure. Most homeowners fall into predictable ranges that help you understand what to expect in today’s market.

| Home Value | Standard Homeowners Premium | With Wildfire Exposure | Earthquake Add-On |

| $750,000 | $1,800 – $2,800/year | $2,800 – $4,500+ | $1,200 – $2,500 |

| $1,000,000 | $2,500 – $4,000/year | $4,000 – $6,500+ | $1,800 – $3,500 |

| $1.5M+ | $4,000 – $7,500/year | $6,500 – $12,000+ | $3,000 – $6,000 |

What Drives Your Final Price?

Your premium depends on Fire Hazard Severity Zone classification (Very High vs Moderate). Roof age and material matter enormously; Class A fire-resistant roofing qualifies for discounts. Rebuild cost per square foot ($350-450+ in Orange County) is what insurers use—not market value.

Your claims history, deductible structure, and whether you use FAIR Plan versus standard carriers all affect your final price. Adding flood or earthquake coverage increases costs but closes critical gaps.

Insurance Availability When Private Carriers Won’t Cover You

If you’ve shopped around and found carriers declining you or offering expensive quotes, you’re not alone. The California FAIR Plan exists specifically for this situation—it’s the state’s insurer of last resort. The FAIR Plan provides basic fire coverage, though it’s more expensive than standard insurance and more limited in scope.

If you’re directed toward the FAIR Plan, work with an independent agent to verify it’s truly your only option. Sometimes persistence and carrier relationships can find standard coverage where online quotes show no options available.

How Old Harbor Insurance Helps Fullerton Homeowners

At Old Harbor Insurance, we start by understanding your property’s specific risks: Fire Hazard Severity Zone classification, proximity to flood zones, earthquake vulnerability, home age and construction, and your financial capacity to handle deductibles. Then we work our carrier relationships to find you coverage that actually fits your situation.

We also help you understand the gaps: where you need additional coverage like flood or earthquake, which mitigation investments can lower your premiums, and how to structure deductibles and coverage limits. Our job is to make sure you’re protected without overpaying for coverage you don’t need.

Protect Your Home and Your Future Today

Your Fullerton home is likely your largest financial investment. Protecting it with insurance that covers your actual risks isn’t optional—it’s essential. The good news is that with the right guidance, you can find adequate coverage at reasonable cost, even in today’s challenging market.

Getting started takes just one conversation. Contact Old Harbor Insurance at (951) 297-9740, email info@oldharbor.com, or get a quote online. One of our agents will review your coverage, identify gaps, and build a protection plan that matches your home and risks. We’re here to give you peace of mind.

Frequently Asked Questions

What should I do if I’m in a Very High Fire Hazard Zone?

If you’re in a Very High Fire Hazard Zone, focus on making fire mitigation improvements that carriers recognize. The California Department of Insurance’s Safer from Wildfires program outlines specific steps like fire-resistant roofing and defensible space. Work with an independent agent who can access carriers willing to write fire-hazard properties and offer discounts for mitigation work.

Why is my homeowners insurance so much more expensive than my neighbor’s?

Location matters more than almost any other factor. Your home’s Fire Hazard Severity Zone, proximity to flood zones, earthquake risk assessment, and even local building codes can affect your premium significantly. Home age, construction materials, roof condition, and claims history also influence rates. An independent agent can explain exactly what’s driving your specific rate.

Do I need separate earthquake insurance if I have homeowners insurance?

Yes. Standard homeowners insurance does not cover earthquake damage. Earthquake insurance is sold separately and comes with a higher deductible. Given Fullerton’s seismic activity, many homeowners opt for at least some earthquake coverage, though the cost-benefit analysis depends on your home’s value and your financial situation.

What happens if I can’t find a carrier willing to insure my Fullerton home?

The California FAIR Plan is available as a last resort, providing basic fire coverage when private insurers decline you. However, FAIR Plan coverage is limited and doesn’t include liability or other perils. Work with an independent agent—sometimes persistence and carrier relationships can unlock options that don’t appear in online quotes.

How often should I review my homeowners insurance policy?

Review your policy annually or whenever you make significant home improvements, complete fire mitigation work, or experience major life changes. Coverage gaps and mitigation improvements that qualify for discounts change over time, so regular reviews ensure your protection stays current.

What’s the difference between replacement cost and actual cash value coverage?

Replacement cost reimburses you the full amount to repair or rebuild your home and replace damaged items at current prices. Actual cash value considers depreciation and pays what the damaged property was worth at the time of the claim. Replacement cost coverage costs more but provides better protection.

Can I lower my homeowners insurance costs without reducing coverage?

Yes. Installing fire-resistant roofing, creating defensible space, adding home security systems, bundling policies, and maintaining a clean claims history can all lower your premiums. Ask your agent about specific discounts your carrier offers for fire mitigation improvements or other safety measures—many offer 5-15% reductions for verified upgrades.