Riverside homeowners face a unique insurance market shaped by seismic risk and wildfire exposure. Standard coverage often leaves critical gaps that most homeowners don’t discover until a claim is denied or they find themselves severely underinsured. That’s why partnering with a local independent agent like Old Harbor Insurance is practical protection.

Understanding what Riverside homeowners need to know about insurance decisions, coverage gaps, and money-saving strategies is the first step toward smart protection. Keep reading to discover exactly how to stop overpaying.

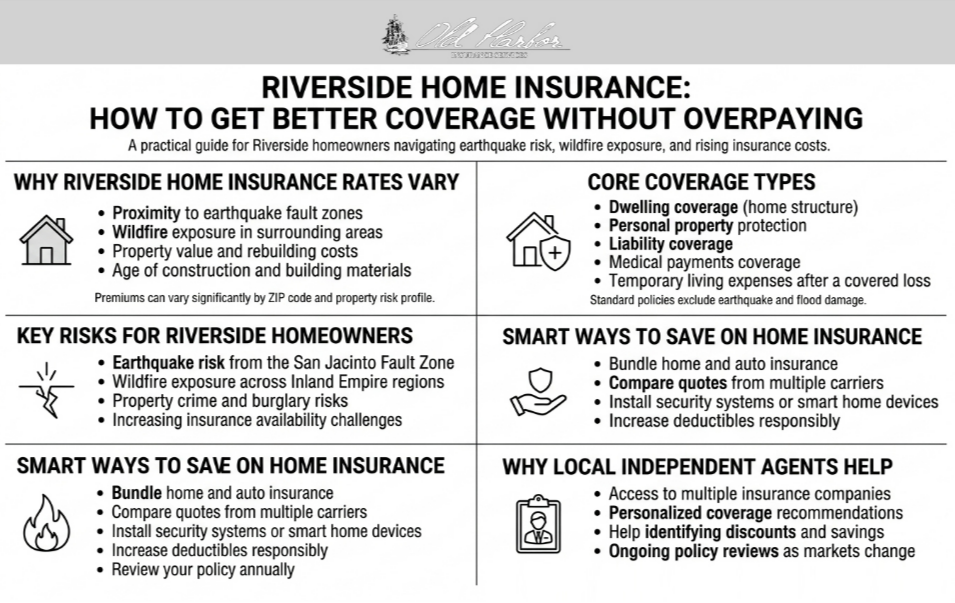

Understanding Riverside Home Insurance Costs

The average homeowners policy in Riverside costs approximately $1,940 per year for $300,000 in coverage with a $1,000 deductible. But this number masks dramatic variation—ZIP code 92509 sees rates around $1,301 annually, while other neighborhoods average nearly $2,000.

What drives variation? Property value, age of construction, proximity to fault lines, and historical loss data all influence premiums. A $300,000 policy with lower deductibles might cost $2,644 yearly, while the same home with a $2,500 deductible drops to $698. Understanding these variables helps you make strategic choices.

Why Riverside Properties Demand Specialized Insurance Planning

Riverside sits in one of California’s highest-risk seismic zones. The San Jacinto Fault Zone runs through the region and is capable of producing 7.0+ magnitude earthquakes. Standard homeowners policies exclude earthquake damage entirely, leaving thousands with a dangerous coverage gap.

Beyond seismic risk, residential burglary rates exceed 11,000 annually, and wildfire zones surround the area. When coverage becomes difficult to find, the California FAIR Plan provides a safety net for homeowners who can’t secure private market policies. Proactive planning now prevents future coverage crises.

Essential Coverage Components for Riverside Homes

Dwelling Coverage: Protecting Your Home’s Structure

Dwelling coverage protects your home’s physical structure—walls, roof, foundation, and attached garage. This must reflect replacement cost, not market value. In Riverside, rebuilding costs have climbed significantly due to labor and materials.

Most Riverside homes require $250,000-$400,000 in dwelling coverage. Your agent should conduct a replacement cost analysis specific to your property, accounting for current construction costs and local building codes. Accurate coverage protects your financial future after a catastrophic loss.

Personal Property Protection: Your Belongings Matter

Personal property coverage reimburses you for furniture, appliances, electronics, and clothing damaged or stolen. Coverage typically maxes at 50-70% of your dwelling limit. High-value items like jewelry or art need separate scheduling for full protection. Understanding these limits prevents unpleasant surprises after a loss.

Liability and Medical Payments Coverage

Liability protects you legally if someone is injured on your property or you accidentally damage theirs. Given Riverside’s demographics, this protection shields your assets from lawsuits. Medical payments coverage handles immediate medical costs for injuries on your property. These protections are often overlooked but critically important.

Earthquake and Flood Insurance Add-Ons

Standard policies exclude earthquake damage. The California Department of Insurance explains earthquake coverage options, and the California Earthquake Authority provides standalone policies. Flood damage also requires separate policies through the National Flood Insurance Program. These additional coverages fill essential protection gaps.

The Local Independent Agent Advantage

Why Multiple Carriers Matter More Than You Think

Independent agents represent dozens of insurance companies, not just one. This means they compare rates and coverage options across multiple carriers simultaneously. One client might qualify for a carrier another agent never considers—creating $300-500 annual savings through carrier diversity.

Old Harbor Insurance serves Riverside homeowners by leveraging relationships with A-rated carriers across California. We understand which companies price competitively in your ZIP code and which ones to avoid. Our agent network provides access to specialty markets and carriers that direct insurers never offer.

Personalized Service Rooted in Your Community

Independent agents invest time understanding your specific circumstances, property details, and financial goals. They assess your home’s age, materials, safety features, and risk exposure before recommending coverage. This personalized approach prevents both underinsurance and overpaying.

Unlike automated online quotes, real conversations surface important details like security systems, recent roof updates, or pools. These details dramatically impact pricing and help reduce premiums legitimately. Your agent becomes a partner who advocates for you year after year.

Strategic Deductible Selection for Riverside Homeowners

Your deductible choice directly impacts your monthly premium. A $500 deductible on a typical Riverside home costs roughly $2,023 annually, while increasing to $1,000 drops premiums to approximately $1,940. That’s $83 in annual savings—but only if you can comfortably pay $1,000 out-of-pocket.

Higher deductibles aren’t universally better. Choose amounts you can genuinely afford without financial strain. An agent helps you stress-test your decision by exploring what happens if you file a claim immediately. The right deductible balances your budget with adequate emergency savings.

Proven Cost-Reduction Strategies

Bundle for Substantial Savings

Bundling homeowners and auto insurance typically saves 11-16% on combined premiums. Independent agents compare bundled pricing across multiple carriers—not all offer equal bundling discounts. Shopping bundled rates with professional guidance often reveals savings direct shopping misses.

Leverage Smart Home Technology

Alarm systems, smart locks, and fire detection devices increasingly trigger insurance discounts. Some carriers reward smart home technology with 5-10% premium reductions. Your agent knows which specific technologies each carrier recognizes and rewards.

Shop Annually, Not Just Once

Insurance markets shift constantly. Carrier pricing changes, new discounts emerge, and your circumstances evolve. Annual policy reviews with your agent uncover new savings opportunities and identify coverage gaps created by life changes.

Choosing the Right Coverage for Your Riverside Home

Start by assessing your actual assets and replacement needs. List your home’s replacement cost, inventory personal property, and consider liability exposure. Compare quotes across carriers before deciding—no two policies are identical.

Understanding what residential insurance covers under California regulations helps you evaluate policy differences. Coverage breadth, exclusions, and rider availability vary significantly between carriers. Take time comparing options rather than rushing into the first available quote.

Common Riverside Home Insurance Misconceptions

Misconception: Standard homeowners insurance covers earthquakes. Reality: It doesn’t. Earthquake coverage requires separate policies, which California Proposition 103 regulates for rate approval.

Misconception: Flood damage is covered under typical policies. Reality: Flood is a standard exclusion. Separate flood insurance is essential in flood zones.

Misconception: All insurance companies price identically. Reality: Rates vary dramatically by carrier and risk assessment methodology.

Misconception: Maximum coverage means maximum protection. Reality: Strategic coverage means appropriate limits without overpaying.

How Old Harbor Insurance Helps Riverside Homeowners

At Old Harbor Insurance, we listen first. We take time understanding your specific circumstances, property details, and financial constraints before recommending coverage. Our independent approach means we shop multiple carriers on your behalf—something direct insurers never do.

We’ve helped hundreds of Inland Empire homeowners navigate Riverside’s unique insurance landscape. Our agents understand seismic risks, wildfire exposure, and the specific challenges Riverside properties face. See what Riverside homeowners say about working with us.

Start Your Riverside Home Insurance Journey Today

Most Riverside homeowners leave hundreds of dollars on the table every year simply because they’ve never shopped with a true independent agent. One call to Old Harbor Insurance reveals what you’re actually missing in coverage and pricing. Get your personalized quote in minutes—our team responds within 24 hours with competitive options.

Take the next step today. Call (951) 297-9740, email info@oldharbor.com, or contact our team. Better coverage and genuine peace of mind are just one conversation away.

Frequently Asked Questions

What’s the average home insurance cost in Riverside?

The average is approximately $1,940 per year for a $300,000 policy with a $1,000 deductible. However, costs vary significantly by ZIP code, home age, and individual property characteristics. Your specific rate depends on your unique situation.

Do I need earthquake insurance in Riverside?

Yes. Standard homeowners policies exclude earthquake damage, and Riverside’s location near the San Jacinto Fault Zone makes this coverage essential. Standalone earthquake policies are available and relatively affordable given the protection they provide.

Should I increase my deductible to save money?

Higher deductibles lower premiums, but only if you can afford to pay the deductible out-of-pocket without financial hardship. Choose a deductible that balances savings with your actual emergency fund capacity.

Why use an independent agent instead of shopping directly?

Independent agents access multiple carriers simultaneously, compare rates and coverage across companies, identify discounts you’d miss alone, and provide ongoing support. They’re your advocate, not a single company’s sales representative.

What discounts can reduce my Riverside home insurance rates?

Common discounts include bundling auto and home policies, installing security systems or smart home devices, maintaining a claims-free history, paying annually instead of monthly, and qualifying for loyalty rewards. Your agent identifies which discounts apply to your specific profile.

What happens if an insurer cancels my policy due to wildfire risk?

The California Insurance Commissioner’s one-year moratorium protects residents in fire-affected areas from cancellation. However, this protection is temporary. If you’re in a high-risk zone, discuss long-term coverage planning with an agent now.

When should I review my homeowners insurance policy?

Review annually and immediately after major life changes like home improvements, property additions, or significant asset changes. Market conditions shift, new coverage options emerge, and your circumstances evolve—all reasons to reassess annually.