San Marcos homeowners face unique coverage challenges that generic insurance guides completely miss. Nestled in North County San Diego’s rolling hills, your property faces wildfire exposure, flood risks from heavy rainfall, and earthquake threats. Most homeowners discover coverage gaps only after a claim is denied. That’s where a local independent agent like Old Harbor Insurance becomes invaluable.

This guide walks you through what San Marcos homeowners actually need to know about coverage, local risks, and proven strategies to protect your property without overpaying. Keep reading to understand exactly how to make informed decisions for your North County home.

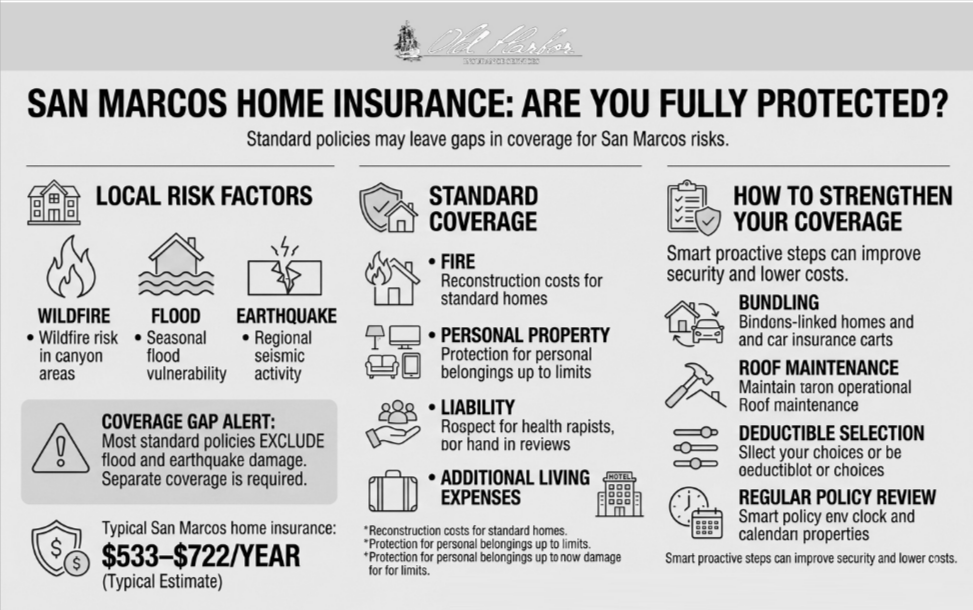

The San Marcos Coverage Challenge

While California doesn’t legally mandate homeowners insurance, every mortgage lender does. Before closing on your San Marcos property, you’ll need “proof of insurance” showing adequate coverage. Your lender requires this because your home secures their loan.

Most lenders require minimum dwelling coverage to rebuild your home. However, covering the minimum isn’t always smart—North County San Diego property values keep rising, meaning rebuilding costs climb too. Understanding your actual replacement cost, not just your home’s market value, is critical for proper protection.

Your Home’s Exposure: Fire, Flood, Earthquakes

San Marcos sits in a region where multiple perils converge. Wildfire risk from surrounding areas means understanding your home’s exposure is critical. Standard policies cover fire damage, but verifying adequate limits and understanding exclusions matters. Some carriers require additional endorsements in high-risk zones.

Flood risks also exist from heavy rainfall and drainage issues unique to North County San Diego. Additionally, home age dramatically affects rates—older San Marcos homes cost up to 57% more to insure than new construction due to increased risk of system failures and weather vulnerability. Understanding these local factors helps you anticipate what coverage you’ll need.

Coverage That Actually Protects You

Dwelling Protection and Personal Property

Dwelling coverage protects your home’s physical structure from fire, windstorms, vandalism, and covered perils. In San Marcos, where wildfire risk exists and property values remain high, ensuring adequate dwelling coverage is essential. Your limit should reflect replacement cost in today’s market, not your home’s purchase price.

Personal property coverage protects belongings inside your home—furniture, electronics, clothing, and valuables. This typically covers 50-70% of your dwelling limit. For high-end items or specialized equipment, additional riders extend coverage for collectibles or custom investments.

Liability and Living Expense Coverage

Liability protection shields you if someone is injured on your property or you accidentally damage theirs. This coverage pays medical bills, legal expenses, and settlements if you’re found responsible. North County San Diego’s higher cost of living means adequate liability limits are particularly important.

Additional Living Expenses (ALE) coverage pays for temporary housing if a covered loss makes your home uninhabitable. Most policies cover approximately 20% of your dwelling limit. Reviewing this amount based on North County San Diego’s rental costs ensures stability during displacement.

Protection Beyond Standard Policies

Flood Insurance Requirements

Standard homeowners policies exclude flood damage entirely, yet San Marcos experiences flood risks from heavy rainfall and drainage issues. The official California homeowners insurance guide explains coverage gaps clearly. Separate flood insurance through the National Flood Insurance Program provides essential protection.

Earthquake Coverage

California earthquake insurance requires separate policies since standard coverage explicitly excludes seismic activity. The California Earthquake Authority provides residential earthquake options for North County homeowners. This protection is prudent given California’s seismic activity.

Wind and Hail Considerations

Wind and hail events impact North County San Diego regularly. While standard policies typically cover these, reviewing wind/hail deductibles ensures adequate protection—some policies feature separate, higher deductibles for these specific perils. Understanding these details prevents surprises during claims.

Finding Better Rates in North County

Independent Agents Access Multiple Carriers

Independent agents represent dozens of insurance companies, not just one. This means comparing rates and coverage options across multiple carriers for your specific San Marcos property. One carrier might price competitively in your neighborhood while another doesn’t serve your area.

Old Harbor Insurance serves North County San Diego with extensive local expertise. We understand San Marcos’s unique risks, know which carriers price fairly in your area, and maintain relationships with A-rated companies. This local intelligence saves tremendous time and money compared to shopping independently.

Smart Bundling and Discount Strategies

Bundling home and auto insurance typically saves 11-16% on combined premiums. Independent agents compare bundled pricing across multiple carriers to find the best combined rates available. Many homeowners are shocked at the savings bundling reveals when professional shopping is involved.

Regular home maintenance also reduces premiums. Roof maintenance is particularly important—insurers reward homes with excellent roof condition with lower rates. Updated electrical wiring, HVAC servicing, and plumbing upgrades also qualify for discounts with many carriers. These improvements pay dividends in lower premiums.

Strategic Deductible Selection

Choosing a higher deductible reduces monthly premiums, though you’ll pay more out-of-pocket during claims. This strategy works well for homeowners with good claims histories and adequate emergency savings. Balance premium savings against your actual financial capacity to ensure the choice makes sense.

San Marcos homeowners can save $250+ by comparing quotes from multiple carriers. Working with an independent agent provides access to multiple companies simultaneously, eliminating the need to contact each carrier separately. Professional shopping saves tremendous time and effort.

When Standard Coverage Isn’t Available

When private insurers deny coverage or exit markets, the California FAIR Plan provides fire-only insurance as a safety net. This state-backed program ensures homeowners in high-risk areas can still obtain coverage, though premiums typically run higher. Understanding these alternatives helps you anticipate options if standard market access becomes difficult.

Proactive planning with a knowledgeable agent prevents insurance crises. Discussing your long-term coverage strategy ensures you’re prepared regardless of market changes.

Credit Scores and Insurance Pricing in North County

Your credit score significantly impacts your insurance rates. Homeowners with poor credit pay up to 46% higher premiums than those with good credit scores. This makes improving creditworthiness one of the most effective cost-reduction strategies available to you.

Interestingly, credit-based insurance scoring considers payment history, outstanding debt, and credit utilization—not the same as traditional credit scores used by lenders. Even if you’re working on improving your credit, discussing this with your agent helps identify carriers with more favorable credit-score policies. Some carriers weigh credit less heavily than others, making professional shopping essential.

How Old Harbor Insurance Helps San Marcos Homeowners

At Old Harbor Insurance, we listen first. We take time understanding your specific circumstances, property details, financial constraints, and local risk exposures before recommending coverage. Our independent approach means we shop multiple carriers on your behalf—something direct insurers never do.

We’ve helped hundreds of North County San Diego homeowners navigate local insurance challenges. Our agents understand wildfire exposure, flood risks, and earthquake considerations specific to San Marcos properties. See what North County homeowners say about partnering with us.

Get Protected Today

Smart coverage for San Marcos doesn’t mean complex research or juggling multiple quotes. A single conversation with one of our agents uncovers protection gaps you’ve likely overlooked and reveals savings most homeowners miss entirely. Get a personalized quote in just minutes—we’ll reach out within 24 hours to discuss your options.

Ready to move forward? Call (951) 297-9740, email info@oldharbor.com, or reach out to us. Your San Marcos property and your family’s security are worth the conversation.

Frequently Asked Questions

Is homeowners insurance required in California?

No, California doesn’t legally mandate homeowners insurance. However, every mortgage lender requires it to protect their financial interest. Even without a loan, maintaining coverage shields you from catastrophic financial loss.

What’s the average cost of home insurance in San Marcos?

San Marcos homeowners typically pay between $533-$722 annually for standard coverage. Individual rates vary significantly based on home age, construction type, location, and coverage selections. Your specific rate depends on your unique property characteristics.

Why does home age impact insurance costs so dramatically?

Older homes present higher risk of system failures, roof leaks, and weather damage. Older San Marcos homes cost up to 57% more to insure than new construction. Roof condition is the single biggest factor—older roofs fail more frequently and cost more to replace.

Do I need separate flood insurance in San Marcos?

Most likely yes. Standard homeowners policies exclude flood damage entirely. Since San Marcos experiences flood risks from heavy rainfall and drainage issues, separate flood insurance is strongly recommended for properties in designated flood zones.

How much can I save by bundling auto and home insurance?

Bundling typically saves 11-16% on combined premiums. For San Marcos homeowners, this often translates to $300-500 in annual savings when compared to separate policies. Independent agents help identify carriers offering the best bundled rates.

Do I need separate earthquake insurance?

Yes. Standard homeowners policies explicitly exclude earthquake damage. Given California’s seismic activity, the California Earthquake Authority provides standalone earthquake coverage. This protection is prudent for North County homeowners given regional seismic risk.

What’s the best strategy for lowering my premiums?

Focus on bundling policies, maintaining your roof and home systems, comparing quotes from multiple carriers, and choosing a deductible you can afford. An independent agent identifies which specific discounts apply to your situation and property.