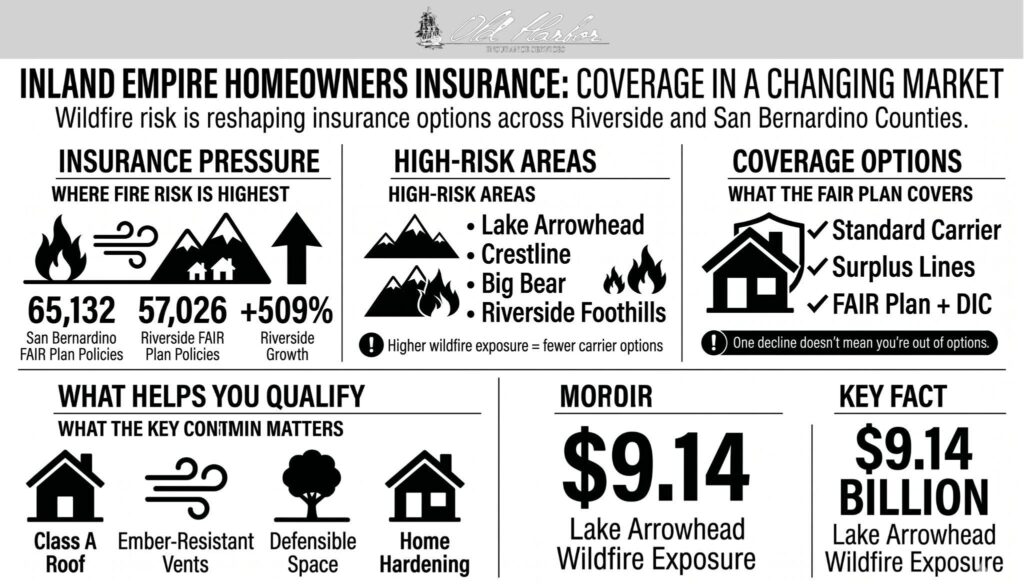

The Inland Empire’s two counties, Riverside and San Bernardino, now hold more FAIR Plan policies than in almost any other part of California. San Bernardino has 65,132 last-resort policies and Riverside 57,026 as of September 2025, with Riverside’s count up 509% in four years, according to MoneyGeek’s analysis of state FAIR Plan data.

For anyone shopping for the best homeowners insurance in the Inland Empire, those numbers explain a lot: standard carriers have pulled back hard, and the policy you can actually buy depends on your address and which company still writes there. Old Harbor Insurance works these conditions as an independent agency rooted in the region.

The best homeowners insurance in the Inland Empire is the policy a carrier will actually write for your specific fire-risk address, which usually means comparing admitted carriers, surplus lines, and the FAIR Plan instead of chasing the lowest advertised rate. A home in the Riverside foothills and one on the Ontario flats can get opposite answers from the same insurer, which is why one quote tells you almost nothing.

What counts as the best homeowners insurance in the Inland Empire

In most places, the best policy is the one that covers you well at the lowest price. In the Inland Empire, the first hurdle is just finding a carrier that will write your address, and write it on terms that hold up when you file a claim.

Inland Empire homeowners pay around the California average of $1,543 a year for $250,000 in dwelling coverage, per MoneyGeek’s analysis of nearly 31 million California quotes, but that figure only applies to homes a standard carrier will still insure.

Three things separate a policy that holds up here from a cheap one that won’t:

- A wildfire answer that actually pays. Either a standard carrier still writing your ZIP code, or a FAIR Plan fire policy wrapped with a Difference in Conditions policy. A bare FAIR Plan policy alone leaves liability, theft, and water damage uncovered.

- Settlement at replacement cost, not actual cash value. Replacement cost rebuilds your home at today’s construction prices; actual cash value subtracts depreciation first and can leave you tens of thousands short on a total loss. In fire country, that line on the declarations page matters more than the premium.

- Earthquake handled on purpose. The Inland Empire straddles the San Andreas Fault system, and no homeowners or FAIR Plan policies cover quake damage. You buy it separately through the California Earthquake Authority or a private carrier, or you carry the risk yourself.

The carrier that clears those three for your address at a price you can live with is the one worth signing, and it is often not a name you would have guessed.

Why Inland Empire coverage got harder

The Inland Empire is not one insurance market. A tract home in Eastvale and a cabin near Lake Arrowhead face completely different underwriting, even though both carry an Inland Empire address. Carriers price the mountain and foothill communities as some of the most exposed property in the state.

The numbers back that up. Lake Arrowhead, Crestline, Big Bear City, and Big Bear Lake all rank among Southern California’s five highest-exposure areas for potential wildfire payout, each carrying between $6.7 and $9.1 billion in FAIR Plan exposure, per CalMatters reporting on the FAIR Plan’s own data. When a carrier sees an address in those ZIP codes, a decline or a non-renewal is often the default.

| Metric | Figure |

| San Bernardino County FAIR Plan policies, Sept 2025 | 65,132 |

| Riverside County FAIR Plan policies, Sept 2025 | 57,026 |

| Riverside four-year policy growth | 509% |

| Lake Arrowhead wildfire exposure | $9.14 billion |

The fire history carriers actually price

Big fires stay in the underwriting models for decades, and the Inland Empire has had its share. The 2003 Old Fire burned more than 90,000 acres in the San Bernardino Mountains, destroyed over 1,000 homes, and killed six people. Carriers still factor that fire into how they rate the mountain communities today.

The recent record is just as active. In September 2024, the Line Fire burned more than 37,000 acres near Running Springs and Big Bear, the Bridge Fire crossed into Wrightwood in San Bernardino County, and the Airport Fire spread from Orange County into Riverside County, as CalMatters documented. After a season like that, carriers in the surrounding ZIP codes raise rates, narrow what they will write, or stop writing altogether.

What changes a “no” into a “yes”

One carrier turning you down does not mean you are out of options. You can still find coverage through admitted carriers, surplus lines, or the FAIR Plan, and which one you land on usually depends on what you can document about the home.

Mitigation is the lever homeowners control. Under California Insurance Code Section 2644.9, any insurer that prices on wildfire risk must offer discounts for documented mitigation, as detailed in the state’s regulatory filing requirements. In the foothill ZIPs, many carriers now treat that work as a condition of getting a quote at all, not just a discount.

| Mitigation step | Why it matters to a foothill underwriter |

| Class A roof | The first thing checked on a mountain-area home |

| Ember-resistant vents | Closes the most common ignition path in wind events |

| 100-ft defensible space | Often required before a carrier will quote |

| Dated clearance photos and receipts | Lets an underwriter approve the file without a site visit |

Riverside and San Bernardino are not the same risk

It is easy to treat the two counties as one, but they price differently, and the spread keeps growing. San Bernardino has more FAIR Plan policies overall, mostly because of mountain towns like Lake Arrowhead, Crestline, and Big Bear, where a single home can have some of the highest fire exposure in the state.

Riverside is catching up fast; its FAIR Plan count jumped 509% in four years, the steepest rise of any large county, as carriers backed away from the foothill communities around the valley. Homeowners in Murrieta or Wildomar are now facing the same problems that a mountain owner faced five years ago.

So a quote from one county tells you little about the other, and even a citywide average hides the street-level split. The carrier that happily writes a flatland home in Fontana may decline one in nearby Lytle Creek. Pull quotes for your exact address from several carriers before you trust any single number.

What the new 2026 laws change

The rules shifted on January 1, 2026, when nine wildfire and insurance laws took effect, per the California Department of Insurance. Two of them matter most if you are deciding whether mitigation is worth the cost: the California Safe Homes Act and the Insurance and Wildfire Safety Act.

The California Safe Homes Act set up a state grant program to help pay for fire-safe roofs and Zone Zero work, the five-foot ember-resistant band around the house that tends to be the most effective and the most expensive step.

For mountain and foothill owners who put off hardening their homes because of the cost, the grant money can cover the part that was holding them back. The Insurance and Wildfire Safety Act requires the state to keep updating its discount rules as the science improves, which should widen the credits available over time.

How Old Harbor Insurance helps

Old Harbor represents 81 A-rated carriers, so an Inland Empire home gets run against the admitted market, surplus lines, and the FAIR Plan in a single pass instead of one carrier at a time. For a homeowner in Crestline or Beaumont, that means a single decline does not automatically send you to last-resort coverage.

The agency also documents mitigation the way underwriters want to see it and explains how each policy behaves when it is time to file a claim after a covered loss, so the file holds together for a lender’s review.

Find the carriers that will write your home

If a carrier already declined or non-renewed you, that is the moment to check your address against the full market rather than assuming the FAIR Plan is the only door left. A standard carrier you never thought to ask may still write the home once it sees the mitigation on file.

Get a quote or contact us to start.

Frequently asked questions

Is the Inland Empire considered high-risk for home insurance?

Parts of it are among the highest-risk in California, especially the San Bernardino Mountains and Riverside foothills. Valley-floor cities like Eastvale and parts of Ontario are rated much lower, which is why quotes vary sharply over short distances.

Why did my Inland Empire carrier non-renew me?

Most non-renewals trace to wildfire exposure scores rather than anything you did. Carriers have been shrinking their books in Riverside and San Bernardino counties as their overall risk concentration in the region climbed.

Does the FAIR Plan cover everything a standard policy does?

No, the FAIR Plan only covers fire, lightning, internal explosion, and smoke. Inland Empire homeowners typically pair it with a Difference in Conditions policy to add liability, theft, and water damage.

Can mountain homes near Big Bear or Lake Arrowhead still get insured?

Yes, though often through surplus lines or the FAIR Plan rather than a standard carrier. Documented home hardening and defensible space materially improve the available options.

Will defensible space actually lower my premium?

State law requires insurers to offer discounts for qualifying wildfire mitigation. Beyond the discount, that work can also be the difference between qualifying for a standard policy and being limited to last-resort coverage.

How many insurers should I compare in the Inland Empire?

Compare as many carriers as will look at your specific address, which in practice means at least three to five and is where an independent agent saves the most time. A single carrier’s decline reflects that one company’s appetite, not the whole market.

Is flood or earthquake covered under an Inland Empire home policy?

No, standard homeowners and FAIR Plan policies exclude both. Given the region’s fault activity, a separate earthquake policy is worth pricing alongside your home coverage.