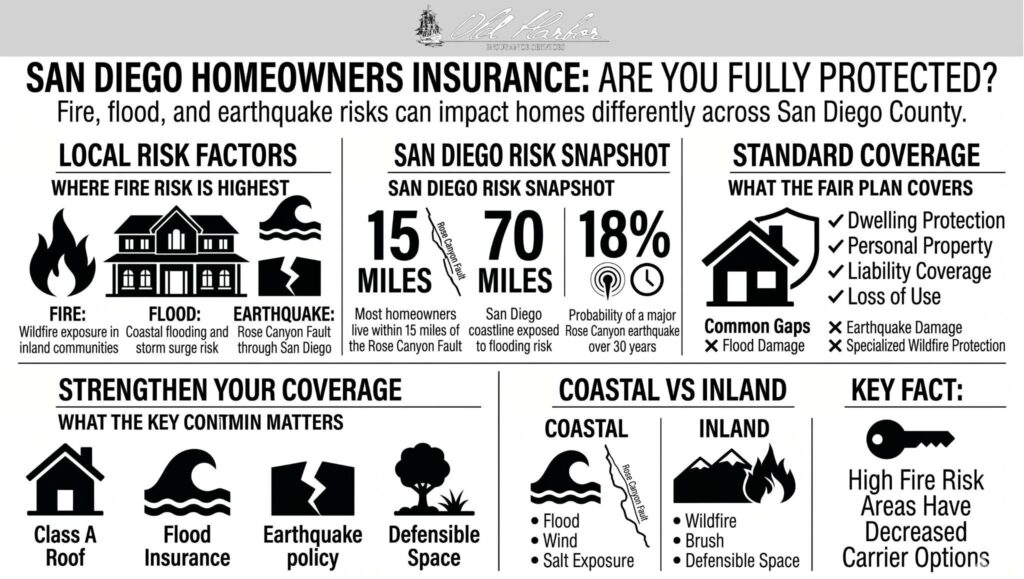

Most San Diego homeowners live within 15 miles of the Rose Canyon Fault, which runs offshore through La Jolla, comes ashore near downtown, and cuts under San Diego Bay, according to the Earthquake Country Alliance.

Between that fault, the brush fires inland, and 70 miles of coastline exposed to flooding, no two San Diego homes carry quite the same risk. Old Harbor Insurance works with homeowners across the county to match coverage to the specific risks at a given address.

A beach condo in Pacific Beach and a ranch in the backcountry face almost nothing in common when it comes to insurance. The two need different things from a policy, and a carrier that writes one cheaply may not write the other at all. Before settling on a quote, it is worth seeing how several carriers price your particular address.

What the best homeowners insurance in San Diego comes down to

San Diego homeowners pay roughly $1,484 per year, slightly below the statewide average, per Insuranceopedia’s San Diego rate analysis. But the average hides a wide spread, and price alone is a poor way to pick a policy here. Three things separate coverage that holds up from a cheap policy that won’t:

- Replacement cost, not actual cash value. With San Diego’s home values and construction costs, a policy that settles at actual cash value subtracts depreciation and can leave you well short of what rebuilding actually costs. Replacement cost is the setting that matters most after a serious loss.

- The right answer for your specific hazard. A coastal home needs flood and wind handled; an inland home needs a real wildfire answer. Few standard policies cover both well, so the gaps get filled with separate policies or endorsements.

- Earthquake, decided on purpose. No homeowners policy covers quake damage, and all of San Diego County sits in the state’s highest seismic zone. It is a separate policy through the California Earthquake Authority or a private carrier, or a risk you carry yourself.

Pick the carrier that covers your address well at a price you can live with. In a market this split, that is usually not the first quote you get back.

Coastal and inland San Diego are different risks

The coast and the backcountry get priced as if they were two separate markets, because they are. Knowing which side of that line your home sits on explains most of what shows up in a quote.

Along the coast, from Ocean Beach and Mission Beach to Coronado, the concerns are flood, wind, and salt exposure. Standard homeowners policies exclude flood damage entirely, so coastal homeowners usually carry a separate flood policy through the National Flood Insurance Program or a private insurer on top of their home policy.

Inland and east, in Poway, Ramona, Alpine, and the rural backcountry, wildfire drives everything. Carriers in those ZIP codes lean heavily on roof type, defensible space, and brush proximity, and a property the coast would routinely insure can be declined a half-hour’s drive east.

The earthquake gap most San Diegans overlook

San Diego’s reputation for seismic calm is misleading. The Earthquake Engineering Research Institute’s San Diego chapter estimated an 18% probability of a magnitude 6.7 or larger quake on the Rose Canyon Fault over a 30-year period, in a scenario study of a 6.9 rupture that modeled damage to roughly 120,000 buildings.

Because the fault runs under the most densely built parts of the county, the exposure sits right where the homes are. Earthquake coverage is bought separately, and the premium depends on your home’s age, foundation, and construction. For an older home, an uninsured quake can wipe out far more than you would ever pay in premiums, which is why it is worth at least getting a price.

Mitigation that changes your options

The same work that lowers risk also reopens carrier options the standard market has closed. Under California Insurance Code Section 2644.9, any insurer that prices based on wildfire risk must offer discounts for documented mitigation, as set out in the state’s regulatory filing requirements.

| Step | Why it matters to an underwriter |

| Class A roof | The first thing checked on an inland or brush-adjacent home |

| Ember-resistant vents | Closes the most common ignition path in wind-driven fire |

| 100-ft defensible space | Often required before a carrier will quote in fire zones |

| Seismic retrofit | Lowers earthquake premiums and damage on older foundations |

| Dated photos and receipts | Lets an underwriter credit the work without a site visit |

How Old Harbor Insurance helps

Old Harbor represents 81 A-rated carriers, so a San Diego home gets checked against the admitted market, surplus lines, and specialty carriers in one pass rather than one company at a time. A coastal condo and a Ramona property on two acres are different problems, and an independent agent can match each to the carriers that actually price it well.

The agency also keeps the home, flood, and earthquake policies aligned, including how each responds when it is time to file a claim after a covered loss, so a loss does not fall through the cracks between them.

Find the coverage that fits your address

If you have been non-renewed, quoted a number that seems off, or just want to know whether you are underinsured, compare your specific address across several carriers instead of renewing on autopilot. A standard carrier you would not have thought to call may write the home for less than you are paying now.

Get a quote or contact us to start.

Frequently asked questions

How much is homeowners insurance in San Diego?

The San Diego average runs around $1,484 a year, slightly below the California average, though coastal and inland homes can land well above or below that. Your rate depends primarily on the dwelling’s value, fire and flood exposure, and the deductible you choose.

Is homeowners insurance required in San Diego?

It is not required by state law, but any mortgage lender will require it as a loan condition. Even without a mortgage, going uninsured in a county with fire, flood, and earthquake exposure is a heavy risk to carry alone.

Does a standard San Diego policy cover earthquakes?

No, earthquake damage is excluded from every standard homeowners policy. Given that the whole county sits in the highest seismic zone and the Rose Canyon Fault runs under the urban core, a separate earthquake policy is worth pricing.

Do I need flood insurance if I live near the San Diego coast?

Likely yes. Standard homeowners policies exclude flood, and coastal neighborhoods from Mission Beach to Coronado carry real surge and flooding exposure that only a separate flood policy addresses.

Why are inland San Diego homes harder to insure than coastal ones?

Wildfire exposure is the reason. Communities like Poway, Ramona, and Alpine sit in higher fire-hazard zones, so carriers there scrutinize roof, brush clearance, and construction far more than they do for a coastal home.

What if no standard carrier will write my San Diego home?

Surplus lines carriers often write properties the admitted market declines, and the FAIR Plan is the fire backstop beyond that. An independent agent can route a hard-to-place home through those markets instead of leaving you uninsured.

Will home hardening lower my San Diego premium?

It can, and state law requires insurers that rate on wildfire risk to offer mitigation discounts. Documented work such as a Class A roof, ember-resistant vents, and defensible space can both lower the premium and broaden the pool of carriers willing to quote.