More than 14 million Californians — over 35% of the state’s population — live in HOA communities, according to Merlin Law Group’s analysis of California common interest developments. The vast majority carry homeowners coverage that was designed without a clear picture of what their HOA’s master policy actually covers. That gap creates real financial exposure, most visibly after water damage, fire, or a large special assessment. Damage that a standard condo insurance policy can close if it’s structured correctly.

Old Harbor Insurance helps San Diego condo owners understand exactly where their HOA’s coverage ends and where their own policy needs to begin, drawing on 81 A-rated carriers to find the right HO-6 structure for their specific building.

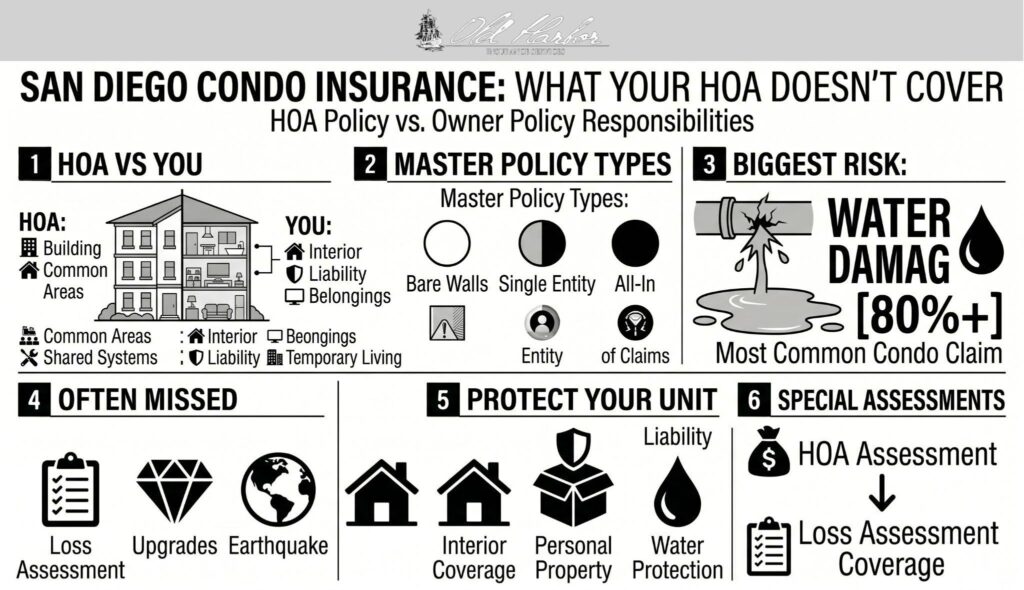

The Three Master Policy Types — and Why They Change Everything

Not all HOA master policies provide the same interior coverage. The type your building carries determines how much dwelling coverage your personal HO-6 policy must include, and many owners discover this only after a loss.

California’s Davis-Stirling Common Interest Development Act requires CC&Rs to define the boundary between HOA-owned common property and individual unit ownership — that document, not your insurance policy, determines who pays for what after a loss.

The three master policy structures are:

| Policy Type | What HOA Covers | What Owner Must Cover |

| Bare Walls | Building shell, exterior, common areas | Everything inside: drywall, flooring, cabinets, fixtures, finishes, personal property |

| Single Entity | Above plus original builder-installed interior finishes | Owner-installed upgrades, personal property |

| All-In | Above plus most interior finishes including improvements | Personal property, liability, loss of use |

Under a bare walls policy — the most limited and increasingly common structure in California as HOA insurance costs rise — an owner is responsible for insuring everything inside the unit from the drywall inward. That includes flooring, cabinetry, countertops, plumbing fixtures, and any upgrades installed by a prior or current owner.

A condo owner who purchases a standard HO-6 policy without knowing their HOA carries bare walls coverage may be significantly underinsured on the dwelling portion alone.

How to Find Out Which Type Your HOA Has

Request a copy of your HOA’s master policy declarations page and CC&Rs from your property management company or HOA board. The declarations page will identify the coverage type. If the policy is unclear, ask specifically whether coverage extends to “original interior finishes within each unit” — that language distinguishes single entity from bare walls.

What Your HO-6 Policy Covers

An HO-6 condo policy is a “walls-in” policy — it covers the interior of your unit, your personal property, your liability exposure, and your living expenses if a covered loss displaces you. The California Department of Insurance outlines the standard components:

- Dwelling (Coverage A): Interior walls, flooring, cabinets, fixtures, and any improvements you’ve made — the scope depends on your HOA’s master policy type

- Personal Property: Furniture, electronics, clothing, and other belongings

- Loss of Use: Hotel stays and living expenses if your unit is uninhabitable after a covered loss

- Personal Liability: Legal defense and damages if someone is injured in your unit

- Medical Payments: Guest injury costs regardless of fault

Understanding how claims are handled under an HO-6 policy before you need to file is particularly important for condo owners, because many losses involve both the HOA’s policy and your own — and coordinating those two claims correctly affects your payout.

Water Damage: The Most Common Condo Coverage Dispute

Water damage claims in multi-unit buildings are the most frequent source of coverage disputes between San Diego condo owners and their HOAs. According to Davis-Stirling’s water damage liability guidance, responsibility depends on the source of the water, who owns the plumbing that failed, and whether negligence was involved.

Who Pays for What

The general framework in California:

- Water damage originating from HOA-owned plumbing (main lines, shared pipes) is typically the HOA’s responsibility to the extent of the building structure; interior damage to your unit may still fall on your HO-6 policy, depending on your master policy type

- Water damage from a pipe inside your unit is typically your responsibility

- Water damage that originated from a neighbor’s unit may be their liability if negligence is established, but proving negligence takes time and a dispute process

- Gradual leaks and seepage are often excluded from both HOA and individual policies

The practical takeaway: never assume water damage from another unit is automatically covered by someone else’s policy. Your HO-6 policy’s water damage coverage and your HOA’s master policy type together determine your actual protection.

Loss Assessment Coverage: The Endorsement Most Owners Skip

When an HOA suffers a large loss — a major fire, roof failure, or lawsuit — and the claim exceeds the master policy limits, the HOA can pass the shortfall to unit owners through a special assessment. These assessments are not covered by a standard HO-6 policy. Loss assessment coverage is an endorsement that specifically covers your share of HOA-levied assessments after a covered event, typically for a modest additional premium.

California’s condo insurance market has made this endorsement more relevant in recent years. As reported by the San Francisco Chronicle, major insurers, including Liberty Mutual, have significantly reduced their California condo building coverage, in some cases slashing coverage limits by 90% or more. When an HOA’s master policy carries far less coverage than the building’s replacement cost, a major loss can generate assessments large enough to financially impact individual owners. A loss assessment endorsement of $50,000–$100,000 can be added to most HO-6 policies for under $50 per year.

Betterments, Improvements, and Upgrades

If you have renovated your kitchen, installed premium flooring, upgraded bathrooms, or added custom built-ins, those improvements are almost certainly not covered under your HOA’s master policy — even under an all-in structure, which typically covers original builder finishes only. Your HO-6 policy’s dwelling coverage needs to reflect the current value of your unit’s interior, including those upgrades.

The Insurance Information Institute’s guidance on HO-6 policies recommends documenting all improvements with photos, receipts, and contractor records and reviewing dwelling coverage limits whenever a significant renovation is completed. Many owners set their HO-6 dwelling limit based on the original purchase price and never update it — leaving upgraded interiors uncovered at replacement cost.

Earthquake and San Diego’s Seismic Exposure

Standard HO-6 condo policies exclude earthquake damage. San Diego County sits near the Rose Canyon Fault, capable of producing significant seismic events.

The California Earthquake Authority offers earthquake coverage specifically designed for condo owners — separate from the building-level earthquake insurance your HOA may or may not carry. Even if your HOA has earthquake coverage on the building structure, your personal property, interior finishes under a bare walls policy, and additional living expenses during displacement are not covered without a personal earthquake endorsement.

How Old Harbor Structures Condo Coverage in San Diego

The right HO-6 policy for a San Diego condo depends on your building’s master policy type, your unit’s improvement value, your personal property volume, and how much loss assessment exposure your HOA carries. Old Harbor Insurance reviews all of those factors before recommending a coverage structure — not just the standard dwelling limit a default quote would generate.

Contact us to review your HOA’s master policy alongside your current HO-6 structure. Get a quote to compare options across the carriers we work with in San Diego.

Frequently Asked Questions

Does my HOA insurance cover everything inside my condo?

It depends on your master policy type. Bare walls policies cover only the building structure and common areas — nothing inside your unit. Single entity policies cover original builder-installed finishes but not owner upgrades. All-in policies cover most interior finishes but not personal property or liability. Request your HOA’s declarations page to confirm which type your building carries.

What is an HO-6 condo insurance policy?

An HO-6 is the standard insurance policy for condo unit owners. It covers the interior of your unit (to the extent your HOA’s master policy doesn’t), your personal belongings, your personal liability, and additional living expenses if a covered loss displaces you. The dwelling coverage limit should be set based on your HOA’s master policy type — bare walls buildings require significantly higher HO-6 dwelling limits than all-in buildings.

Who pays for water damage when a pipe leaks from a neighboring unit?

California follows a negligence-based framework. If the neighbor was negligent — they left a faucet running, failed to report a known leak — they may be liable for damage to your unit. If the failure was sudden and accidental with no negligence, each party typically covers their own interior damage through their respective policies. Your HO-6 water damage coverage provides protection while any negligence dispute is resolved.

What is loss assessment coverage and do I need it?

Loss assessment coverage pays your share of an HOA-levied special assessment after a covered loss exceeds the master policy limits. As California condo building coverage has contracted, the risk of under-covered master policies — and resulting assessments — has grown. Most HO-6 policies can add $50,000 or $100,000 in loss assessment coverage for under $50 per year. It is one of the highest-value endorsements available to condo owners and one of the least commonly carried.

Can my HOA charge me after a major insurance claim?

Yes. If a loss exceeds the master policy limits, or if the HOA’s deductible is large enough to create a shortfall, the board can levy a special assessment on all unit owners to cover the gap. This is increasingly common as California HOA master policies have been cut or priced out of adequate coverage limits. Loss assessment coverage on your HO-6 policy protects against this specific exposure.

Do San Diego condo owners need earthquake insurance?

Standard HO-6 policies exclude earthquake damage. San Diego sits near the Rose Canyon Fault, and earthquake risk in the region is real. The California Earthquake Authority offers condo-specific earthquake policies covering personal property, interior finishes under bare walls policies, and additional living expenses during displacement. Whether your HOA carries earthquake coverage on the building structure is a separate question — it doesn’t protect your unit’s interior or your personal property without a personal policy.

What documents should I review before buying condo insurance?

Request and review three documents: your HOA’s master policy declarations page (to identify the coverage type), your CC&Rs (to understand maintenance and insurance obligations), and any recent HOA board minutes referencing special assessments or insurance changes. Those three documents together give a complete picture of where the HOA’s coverage ends and where your personal HO-6 policy must begin.