The California FAIR Plan has grown from a niche last-resort program to a primary insurance mechanism for hundreds of thousands of homeowners. As of March 2025, the plan carried 573,739 policies — up 74% since September 2023 and 139% since September 2021, according to Insurify’s analysis of FAIR Plan data. The plan was designed as a temporary safety net. For many Californians, it has become a multi-year permanent placement — and that creates real coverage gaps that most policyholders don’t fully understand until they file a claim.

Old Harbor Insurance helps California homeowners understand what the FAIR Plan covers, what it doesn’t, and what alternatives exist in the current market — including paths back to standard coverage that most articles never explain.

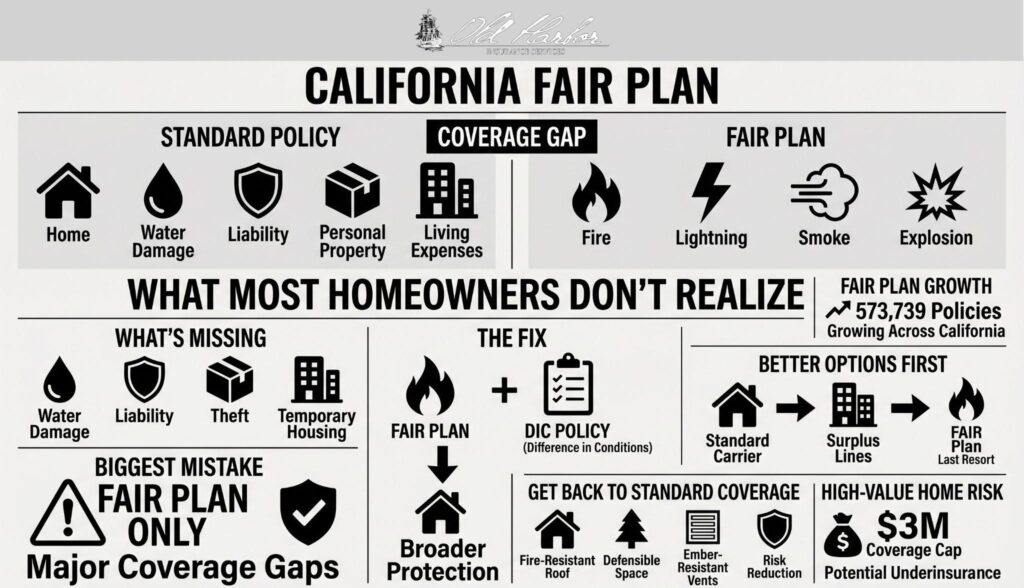

What the California FAIR Plan Actually Covers

The California FAIR Plan provides basic hazard insurance for residential properties that the private market has declined. Standard FAIR Plan coverage includes fire, smoke, lightning, and internal explosion. Extended coverage endorsements can add wind, hail, explosion, riot, aircraft, vehicle, and volcanic action for an additional premium.

What the FAIR Plan does not include as standard is equally important. The table below compares a standard homeowners policy with FAIR Plan coverage:

| Coverage | Standard Policy | FAIR Plan |

| Fire and Smoke | Yes | Yes |

| Theft | Yes | No |

| Personal Liability | Yes | No |

| Water Damage (sudden) | Usually Yes | No |

| Additional Living Expenses | Usually Yes | Limited |

| Personal Property (full) | Yes | Limited |

| Earthquake | Separate policy | No |

| Flood | Separate policy | No |

FAIR Plan coverage is capped at $3 million per residential property. For homeowners with high-value properties, that limit alone can create significant underinsurance exposure. The plan also pays out on an actual cash value basis for many claim types rather than replacement cost, which means depreciation is deducted from your payout on older structures and contents.

Why the FAIR Plan Is Growing Beyond High-Risk Areas

The FAIR Plan’s growth is no longer confined to wildland-urban interface communities. According to United Policyholders’ March 2026 analysis, 14% of current FAIR Plan policies and 28% of the plan’s total exposure now sit in largely urban, lower-fire-risk zones. The plan added 21,859 residential policies in Q4 2025 alone — more new policies in a single quarter than California’s Sustainable Insurance Strategy has committed to writing in two years across the entire state.

According to the California Department of Insurance’s wildfire and insurance data, carrier non-renewals and FAIR Plan policy growth are tracked together as companion indicators of market distress. Both have moved in the same direction since 2019. The average FAIR Plan policyholder has been enrolled for five and a half years — well beyond the plan’s intended temporary role — and those in lower-risk urban areas average closer to seven years of continuous enrollment.

The Difference in Conditions Policy: Essential Pairing

Most homeowners on the FAIR Plan don’t realize the coverage gaps they’re carrying until they file a claim. A Difference in Conditions policy is a supplemental policy specifically designed to fill what the FAIR Plan excludes — liability protection, water damage, theft, and additional living expenses coverage for temporary housing after a covered loss.

What a DIC Policy Adds

A properly structured FAIR Plan plus DIC combination approximates the breadth of a standard homeowners policy. Without a DIC policy, a FAIR Plan policyholder has no liability protection if someone is injured on their property, no coverage for a burst pipe flooding their kitchen, and no reimbursement for hotel stays if their home becomes uninhabitable after a fire.

Understanding how claims are handled under each policy structure before you need to file is the most practical step any FAIR Plan policyholder can take. The cost of a DIC policy varies by carrier and coverage scope, but it is significantly less expensive than the gaps it covers would cost to absorb out of pocket.

Alternatives to the FAIR Plan

The FAIR Plan should be the last option evaluated, not the first. Two market tiers exist between a standard admitted policy and the FAIR Plan.

Standard Admitted Carriers

Despite well-documented pullbacks, dozens of admitted carriers continue writing California homeowners policies. Some that restricted new writing during 2022–2024 have returned selectively under the Sustainable Insurance Strategy reforms, which allow carriers to use forward-looking wildfire models and recover reinsurance costs in their rates in exchange for commitments to write more policies in high-risk areas.

The California Department of Insurance provides a home insurance finder tool that lists carriers currently writing policies in California — a resource many homeowners never consult before accepting FAIR Plan placement.

Surplus Lines Carriers

Non-admitted (surplus lines) carriers operate outside California’s rate-regulation framework, giving them flexibility to write properties that admitted carriers decline. They are not backed by the California Insurance Guarantee Association, and premiums are typically higher, but coverage can be comprehensive and significantly broader than the FAIR Plan without requiring a separate DIC policy.

For properties in high fire-risk zones that the standard market has declined, surplus lines is almost always worth exhausting before defaulting to the FAIR Plan structure. The California Department of Insurance explicitly references surplus lines as an alternative path when admitted coverage is unavailable.

How to Move Off the FAIR Plan

The section most competitors skip is how to get out of the FAIR Plan once you’re on it. Returning to the voluntary market requires demonstrating reduced risk, and California now gives insurers specific financial incentives to take FAIR Plan policyholders back.

Home Hardening and Mitigation

California’s Safer from Wildfires framework requires admitted insurers to offer premium discounts for documented wildfire mitigation. These same improvements shift a property’s risk score in carrier underwriting models, improving eligibility with carriers that previously declined. The highest-impact steps are: Class A fire-resistant roofing, ember-resistant vents, 100 feet of defensible space, and fire-resistant siding. Each improvement should be documented through a defensible space inspection report from your county fire district — insurer credit requires verified documentation, not self-reported upgrades.

Working With an Independent Agent

An independent agent who re-shops your coverage annually will catch market conditions that self-service tools miss. Under the Sustainable Insurance Strategy, carriers, including Farmers, CSAA, and Mercury, have committed to writing new policies in high-risk areas.

CSAA has already reported writing 18,300 more policies in high-hazard areas than required. These commitments create openings that didn’t exist two years ago — but they require an agent who tracks which carriers are actively accepting FAIR Plan transitions in your ZIP code.

Recent FAIR Plan Reforms California Homeowners Should Know

The California Department of Insurance issued 2026 guidance addressing FAIR Plan claims handling, transparency requirements, and coverage modernization. The plan levied a $1 billion special assessment on member insurers in early 2025 to shore up reserves following the LA fires — the first such assessment in the plan’s history. The assessment will likely be partially passed on to policyholders through market-wide premium adjustments.

FAIR Plan policyholders should also be aware that the plan’s $3 million coverage cap has become a meaningful constraint for higher-value California properties, as rebuild costs in many markets now exceed that threshold.

How Old Harbor Insurance Navigates This Market

Finding the right structure — whether that is a standard policy, a surplus lines placement, or a FAIR Plan plus DIC combination — requires access to all three market tiers simultaneously. Old Harbor Insurance works independently across 81 A-rated carriers to identify what is available for your specific address, how your property profiles against current carrier appetite, and where the best combination of coverage and premium exists right now.

Contact us to review your current coverage structure. Get a quote to see what the market currently offers for your property.

Frequently Asked Questions

Is the California FAIR Plan the same as homeowners insurance?

No. The FAIR Plan provides basic hazard coverage for fire and a limited set of other perils. It does not include liability protection, theft coverage, standard water damage coverage, or adequate additional living expenses protection. Most homeowners pair it with a Difference in Conditions policy to approximate what a standard homeowners policy covers.

What does hazard insurance mean in California?

Hazard insurance refers to the portion of a homeowners policy that covers damage to the structure from specific perils — fire, wind, hail, and similar events. In California, the term is often used interchangeably with homeowners or dwelling insurance, though lenders sometimes specify hazard insurance as the minimum coverage required to satisfy a mortgage requirement.

Does the FAIR Plan cover liability?

No. Premises liability protection — coverage for legal defense and damages if someone is injured on your property — is not included in the FAIR Plan. A Difference in Conditions policy or a separate liability policy is needed to fill this gap. Without it, a FAIR Plan policyholder bears all personal liability exposure from property-related injuries or incidents.

Can I switch from the FAIR Plan back to traditional homeowners insurance?

Yes, and it is more achievable now than in recent years. Documented wildfire mitigation improvements, updated roof materials, and defensible space compliance all shift your property’s risk profile favorably. Under the Sustainable Insurance Strategy, several carriers have made active commitments to write policies in high-risk areas. An independent agent who tracks current carrier appetite in your ZIP code is the most reliable path back to the voluntary market.

Are surplus lines insurers a safe alternative to the FAIR Plan?

Generally yes, with one important distinction. Surplus lines carriers are not backed by the California Insurance Guarantee Association, meaning you do not have CIGA’s insolvency protection if the carrier fails. For that reason, confirming the carrier’s financial stability rating before binding coverage is important. With that check done, surplus lines typically offer broader coverage than the FAIR Plan at lower total cost than a FAIR Plan plus DIC combination.

Does the FAIR Plan cover water damage?

Not under the base policy. The FAIR Plan covers fire, smoke, lightning, and internal explosion as standard perils. Extended endorsements add some weather-related perils, but sudden water damage from burst pipes or appliance failures — a standard covered peril under traditional homeowners policies — is not included. A DIC policy paired with the FAIR Plan typically fills this gap.

How can I find out if a standard carrier will insure my property?

The California Department of Insurance offers a home insurance finder tool at insurance.ca.gov that lists admitted carriers currently writing policies in the state. An independent agent with access to both admitted and surplus lines markets can run your specific property profile across the full range of options simultaneously — a more thorough search than any single-carrier or self-service tool provides.