San Marcos sits in one of North County San Diego’s fastest-growing housing markets, where median home values now exceed $750,000 according to U.S. Census Bureau data. That growth creates a specific insurance challenge: homes are worth more, cost more to rebuild, and sit in a region where wildfire and flood exposure affect both carrier availability and premiums. A policy that was adequate three years ago may no longer reflect what your property would actually cost to replace.

Old Harbor Insurance works with North County San Diego homeowners across 81 A-rated carriers to find coverage calibrated to what San Marcos properties actually face, rather than a generic Southern California rate.

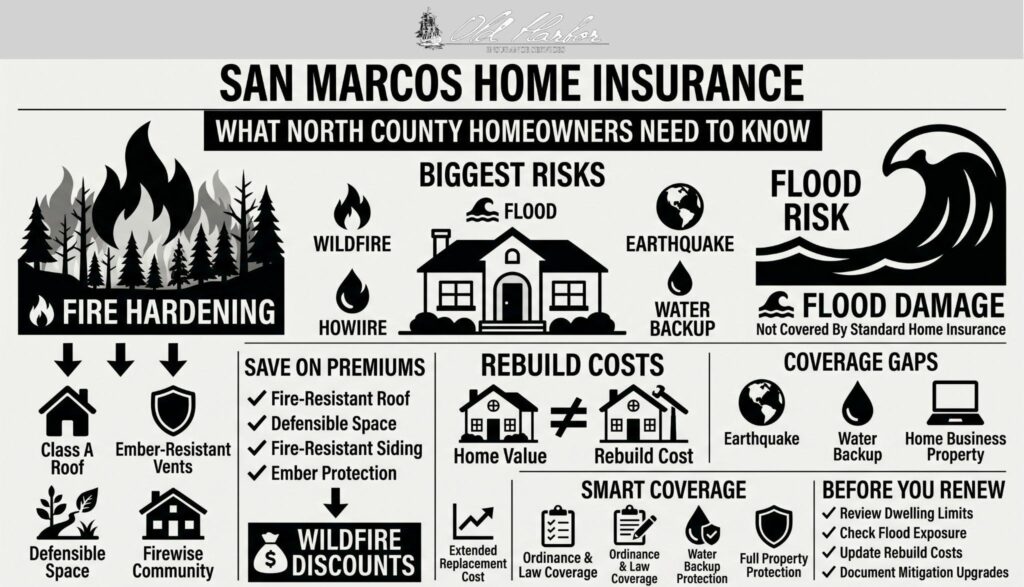

San Marcos Wildfire Exposure: What the New Maps Show

The City of San Marcos published updated Fire Hazard Severity Zone maps in March 2025, incorporating revised climate data, fuel load modeling, and ember spread analysis that expanded zone boundaries across many North County communities from the previous 2009 maps. Properties near Elfin Forest, San Elijo Lagoon, and the eastern foothills are most likely to carry High or Very High designations.

Zone classification is only part of how carriers assess risk. As the California Department of Insurance clarified in its 2025 FHSZ guidance, insurers use their own property-level scoring that factors in slope, vegetation density, proximity to fire suppression, and construction materials—not zone maps alone. The San Diego Fire Department’s wildfire hazard guidance provides additional regional context on North County’s wildland-urban interface conditions.

How Wildfire Mitigation Can Lower Your Premium

California requires admitted insurers to offer premium discounts for documented wildfire mitigation improvements under the Safer from Wildfires framework. This is one of the least-discussed tools available to San Marcos homeowners, and it creates a direct financial return from investments that also reduce actual fire risk.

Improvements That Qualify

Qualifying improvements under California’s wildfire discount regulations include:

- Installing a Class A fire-resistant roof

- Replacing combustible wood vents with ember-resistant alternatives

- Maintaining at least 100 feet of defensible space with documented vegetation clearance

- Replacing combustible siding and decking with fire-resistant materials

- Participation in a Firewise USA or similar community wildfire mitigation program

Each qualifying improvement earns a separate discount under the framework. Homeowners who complete multiple improvements can compound those discounts significantly. Documentation through a county fire district defensible space inspection is the most reliable way to ensure the improvements register in carrier underwriting.

Flood Risk in San Marcos: More Than You Might Expect

Standard homeowners policies do not cover flood damage from any external water source. San Marcos has more flood exposure than many homeowners realize, concentrated in neighborhoods near Richland Creek, San Elijo Creek, and the drainage corridors that run through the city’s lower-elevation areas.

Homeowners can check their specific address using both the FEMA Flood Map Service Center and San Diego County’s flood mapping resources, which includes county-maintained drainage channel data that provides more granular local information than FEMA’s national maps alone. Properties near creek corridors or low-lying drainage areas may face meaningful flood exposure even when officially outside a designated Special Flood Hazard Area. Separate flood coverage is available through FEMA’s National Flood Insurance Program and through private flood carriers that often provide broader terms than the NFIP.

Why Replacement Cost Coverage Matters in This Market

Many San Marcos homeowners insure their property to its market value or the original purchase price rather than its true replacement cost. According to the Insurance Information Institute, underinsurance is among the most frequent and costly gaps homeowners discover after a major loss. In North County San Diego, where construction labor and materials costs have climbed sharply since 2020, the gap between market value and actual rebuild cost can be substantial.

Understanding how claims are settled before a loss is the most practical preparation a homeowner can make. Two specific issues are worth flagging for San Marcos properties. First, extended replacement cost coverage pays a percentage above your dwelling limit if rebuild costs exceed your policy’s stated amount. Second, ordinance and law coverage pays the additional cost of bringing a rebuilt structure up to current California building codes, which have been updated significantly in recent years. Both are worth discussing at every policy renewal.

Coverage Gaps Worth Addressing

Beyond wildfire and flood, several coverage areas are commonly underestimated or excluded from standard San Marcos homeowners policies:

Earthquake:

Standard policies exclude earthquake damage. The California Earthquake Authority provides coverage through participating residential insurers. San Marcos sits within influence of the Rose Canyon and Elsinore fault systems.

Water backup:

Sewer and drain backup is excluded from standard policies but is a common and expensive claim type. A water backup endorsement covers damage from reversed drains or backed-up sewer lines, typically for a modest additional premium.

Home-based business property:

Standard policies apply low sub-limits to business equipment kept at home. Remote workers and home-based business owners with significant equipment should review whether a business property endorsement or separate business policy is needed.

How Old Harbor Insurance Works for San Marcos Homeowners

A captive agent representing a single carrier provides limited options in a market where carrier appetite for North County San Diego properties varies by address, construction profile, and wildfire zone classification.

Old Harbor Insurance works independently across 81 A-rated carriers, comparing the full range of admitted and surplus lines options for your specific property. That market access matters particularly for properties in or near FHSZ boundaries, where the difference between carriers can be significant in both pricing and coverage structure.

Contact us to review your current coverage, or get a quote to see what is currently available for your address.

Frequently Asked Questions

How does San Marcos’s 2025 FHSZ map update affect my homeowners insurance?

The March 2025 update expanded or reclassified some San Marcos properties into higher fire hazard zones based on new modeling. Properties newly designated as High or Very High FHSZ may face stricter defensible space requirements, building code standards for new construction, and closer insurer scrutiny at renewal. The CDI has clarified that the new maps do not automatically cause non-renewals or price increases, but insurers use their own models alongside the official maps.

Is wildfire damage covered by standard homeowners insurance in San Marcos?

Yes. Wildfire is a named peril under standard homeowners policies. Coverage gaps typically arise from underinsured dwelling limits, inadequate extended replacement cost provisions, or insufficient additional living expenses coverage rather than an outright wildfire exclusion. Review your dwelling limit against current North County rebuild costs at every renewal.

Do I need flood insurance in San Marcos?

It depends on your address. Properties near Richland Creek, San Elijo Creek, and other drainage corridors carry real flood exposure even if they are outside FEMA’s designated Special Flood Hazard Areas. Standard homeowners policies do not cover flood damage from external water sources. Checking both the FEMA Flood Map Service Center and San Diego County’s drainage channel maps provides the most complete picture for your specific address.

What is the difference between replacement cost and actual cash value coverage?

Replacement cost pays to rebuild your home at current construction prices without deducting for depreciation. Actual cash value deducts depreciation, so an aging roof or older siding is paid out at a fraction of replacement cost. For San Marcos homes with older construction, the gap between these two settlement approaches on a major claim can be significant. Most carriers offer replacement cost as the standard dwelling settlement option; confirm your policy’s basis before assuming it applies.

Are California insurers required to offer wildfire mitigation discounts?

Yes. Under California’s Safer from Wildfires regulations, admitted insurers must offer premium discounts to homeowners who document qualifying wildfire mitigation improvements. Each qualifying improvement earns a separate discount, and multiple improvements can compound the total reduction. Defensible space, ember-resistant vents, Class A roofing, and fire-resistant siding are among the improvements that qualify. Surplus lines carriers are not subject to the same mandate but increasingly use mitigation documentation in their own property-level risk scoring.

Does a standard homeowners policy cover earthquakes in San Marcos?

No. Earthquake damage is explicitly excluded from standard homeowners policies and requires a separate policy through the California Earthquake Authority or a private earthquake insurer. San Marcos is within seismic influence of the Rose Canyon and Elsinore faults. The CEA offers policies through participating residential insurers, with premium varying based on home age, construction type, and foundation.

What endorsements are most valuable for North County San Diego homeowners?

For most San Marcos properties, the highest-priority endorsements are: extended replacement cost (covers rebuild costs that exceed your dwelling limit), ordinance and law coverage (pays for code-upgrade costs during a rebuild), and water backup coverage. Homeowners near FHSZ boundaries should also review their wildfire deductible structure, since some policies apply a percentage-based wildfire deductible rather than a flat dollar amount, which can mean a significantly higher out-of-pocket cost on a fire claim.