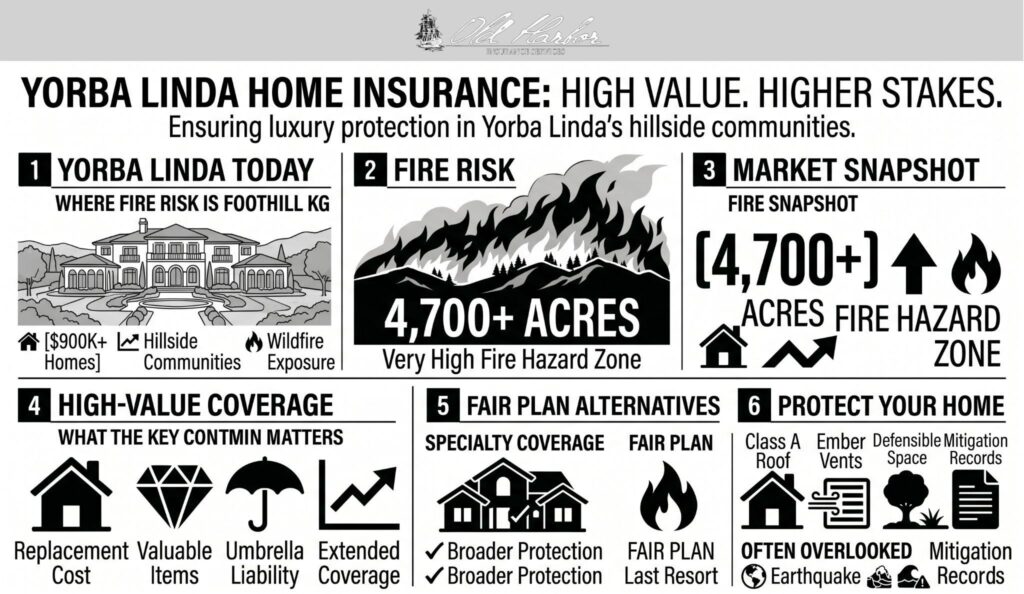

Yorba Linda is one of Orange County’s most affluent communities, with a median home value exceeding $900,000 according to U.S. Census Bureau data. The city’s 2025 fire hazard maps now classify more than 6,500 acres within Moderate, High, or Very High Hazard Severity Zones — with over 4,700 acres in the Very High category alone. For homeowners at that value level and that risk profile, a standard homeowners policy rarely provides adequate protection.

Old Harbor Insurance works with Yorba Linda homeowners across 81 A-rated carriers to find coverage that matches the actual replacement cost and risk exposure of high-value Orange County properties — including admitted, surplus lines, and specialty markets.

Yorba Linda’s Wildfire Exposure: What the 2025 Maps Changed

The updated CAL FIRE Fire Hazard Severity Zone maps released March 24, 2025, marked the first comprehensive revision since 2007. In Yorba Linda, the reclassification was significant: neighborhoods in the city’s hillside areas north of the 91 Freeway, particularly those adjacent to open space and the Chino Hills State Park boundary, are most heavily affected by new Very High designations.

Yorba Linda’s city government has responded proactively. Funded through grants from CAL FIRE and FEMA, the city completed a Local Hazard Mitigation Plan that identifies wildfire, earthquake, and drought as the primary hazard threats. The city, the Orange County Fire Authority, and the Yorba Linda Water District jointly issued a letter homeowners can share with their insurance providers to document the community’s mitigation efforts — a meaningful tool in conversations with carriers about underwriting eligibility.

Why Market Value Is Not the Same as Replacement Cost

The most common and costly insurance mistake Yorba Linda homeowners make is insuring to their property’s market value rather than its true replacement cost. The Orange County Assessor separates land value from structure value in its assessments — and land value, which can represent 40% or more of a home’s market value in Yorba Linda, is not insurable. What matters for coverage purposes is the cost to rebuild the structure at current construction prices.

For Yorba Linda homes with custom finishes, premium materials, and significant square footage, structure-only replacement cost frequently exceeds $500–$700 per square foot. A 3,500-square-foot home with a $1.75 million rebuild cost insured at its $1.2 million market value carries a $550,000 gap that surfaces when a total loss claim is filed. The Insurance Institute for Business and Home Safety documents how post-disaster reconstruction costs routinely spike 20–40% above pre-event estimates when regional rebuilding demand compresses labor and materials supply simultaneously.

Coverage Components High-Value Yorba Linda Homes Need

Extended Replacement Cost

A standard dwelling limit pays up to the stated policy amount. Extended replacement cost coverage adds a percentage buffer — typically 25–50% — above that limit. Guaranteed replacement cost, available through specialty high-value carriers, pays whatever the full rebuild costs, regardless of the stated limit.

For Yorba Linda homes where custom architecture and premium materials drive rebuild costs well above standard valuations, guaranteed replacement cost is the appropriate standard.

Ordinance and Law

California’s building codes have changed substantially since most of Yorba Linda’s established neighborhoods were built. A partial loss on an older structure can trigger code-compliance requirements on undamaged portions — costs that a base policy won’t cover. Ordinance and law coverage pays those additional code-upgrade expenses as part of a covered rebuild, and is particularly relevant for Yorba Linda homes built before the 2000s.

Scheduled Personal Property

Standard policies apply sub-limits of $1,500–$2,500 to categories like jewelry, art, and collectibles. For Yorba Linda homeowners with significant collections — jewelry, watches, wine, fine art, luxury electronics — a scheduled personal property endorsement covers those assets at their appraised value without sub-limit caps, accidental breakage coverage, and in many cases no deductible.

Umbrella Liability

Yorba Linda’s larger lots, pools, and home entertainment spaces create above-average premises liability exposure. Standard homeowners liability limits of $100,000–$300,000 can be exceeded by a single pool incident or guest injury claim in California’s litigation environment. An umbrella policy extending coverage to $2–5 million adds that layer for typically $200–$400 per year.

FAIR Plan Realities for Yorba Linda Homeowners

The California FAIR Plan covers fire, smoke, lightning, and a narrow set of other perils. It does not include liability protection, theft coverage, water damage, or additional living expenses as standard components. Its $3 million dwelling cap creates a structural gap for Yorba Linda properties with rebuild costs above that threshold.

The FAIR Plan should be a last resort, not a first response to a non-renewal. Two alternatives are worth exhausting before defaulting to FAIR Plan enrollment:

- Surplus lines carriers can write properties that admitted carriers decline, often with broader coverage than the FAIR Plan at a lower total cost than a FAIR Plan plus DIC combination

- Specialty high-value carriers (Chubb, AIG Private Client, PURE) access through independent agents who regularly place Orange County luxury properties — these carriers use property-level risk scoring that rewards documented mitigation rather than blanket zone exclusions

If the FAIR Plan does become necessary, it must be paired with a Difference in Conditions policy to fill the liability, water damage, and personal property gaps. Understanding how claims work under the FAIR Plan versus a standard policy is essential before committing to that structure — the claims process differs significantly.

Using Yorba Linda’s Community Mitigation Letter

One practical tool that is unique to Yorba Linda and rarely publicized: the city’s joint letter — produced in collaboration with the OCFA and Yorba Linda Water District — specifically documents the community’s wildfire mitigation programs for use with insurance providers. This letter can be submitted to carriers during underwriting review to demonstrate that Yorba Linda has invested in community-level fire risk reduction. According to California’s Safer from Wildfires framework, insurers are required to recognize both individual property and community-level mitigation efforts in their pricing — making this letter a tangible underwriting tool, not just a goodwill gesture.

Combined with individual property hardening steps — Class A roofing, ember-resistant vents, documented defensible space — Yorba Linda homeowners are better positioned to access and retain admitted market coverage than homeowners in communities without equivalent mitigation infrastructure. The IBHS research identifies ember intrusion through vents and roof vulnerabilities as the two most common wildfire ignition pathways.

Earthquake and Flood: The Often-Skipped Exposures

Standard homeowners policies exclude both earthquake and flood damage. The California Earthquake Authority provides earthquake coverage through participating residential insurers, and Yorba Linda’s proximity to the Puente Hills Fault — which ruptured in 1987 causing $358 million in damage across Orange County — makes seismic coverage worth evaluating carefully for high-value properties.

Flood is a less prominent risk in Yorba Linda than in lower-lying Orange County communities, but properties near the Santa Ana River corridor and Santiago Creek drainage areas carry real flood exposure. Homeowners can check their specific address at the FEMA Flood Map Service Center to confirm designation before deciding whether flood coverage is warranted.

How Old Harbor Insurance Serves Yorba Linda Homeowners

A captive agent representing one carrier provides a ceiling when that company’s underwriting guidelines don’t favor Yorba Linda’s hillside ZIP codes.

Old Harbor Insurance works independently across 81 A-rated carriers — comparing admitted carriers, surplus lines, and specialty programs for your specific address, identifying which carriers currently weigh Yorba Linda’s community mitigation letter favorably, and structuring extended replacement cost and personal property coverage to match what a high-value property actually requires.

Contact us to review your coverage against what the current market offers for your property. Get a quote to compare real options today.

Frequently Asked Questions

Why is homeowners insurance harder to obtain in Yorba Linda than in other Orange County cities?

Yorba Linda’s hillside neighborhoods and proximity to open space place a significant portion of the city within Very High Fire Hazard Severity Zones. Over 4,700 acres now carry the highest risk designation under the 2025 CAL FIRE maps. Insurers use their own proprietary risk models layered on top of these official designations, and properties on upslope terrain near open space face stricter underwriting regardless of individual property characteristics.

What does the California FAIR Plan actually cover for Yorba Linda homeowners?

The FAIR Plan covers fire, smoke, lightning, and internal explosion as standard perils. It does not include liability protection, theft, water damage from burst pipes, or additional living expenses after a covered loss. Its $3 million coverage cap can be inadequate for Yorba Linda properties with rebuild costs above that threshold. Most homeowners using the FAIR Plan should pair it with a DIC policy to fill those gaps.

What is extended replacement cost coverage and why does it matter here?

Extended replacement cost pays a percentage above your stated dwelling limit — typically 25–50% — if rebuild costs exceed your policy limit after a total loss. For Yorba Linda homes with custom features and premium materials, post-disaster rebuild costs can spike well above pre-loss estimates when regional demand compresses labor and materials. Guaranteed replacement cost, available through specialty carriers, provides a higher level of protection with no cap on the final payout.

Do I need earthquake insurance in Yorba Linda?

Standard homeowners policies exclude earthquake damage. Yorba Linda sits near the Puente Hills Fault, which caused significant damage across Orange County in 1987. The California Earthquake Authority offers residential earthquake policies through participating insurers, with premium based on home age, construction type, and proximity to fault systems. For a high-value Yorba Linda property, the financial exposure from an uninsured seismic event justifies serious evaluation.

How does Yorba Linda’s community mitigation letter help with insurance?

The City of Yorba Linda, in collaboration with the OCFA and Yorba Linda Water District, produced a joint letter documenting the community’s wildfire mitigation investments. California’s Safer from Wildfires framework requires admitted insurers to recognize community-level mitigation in their pricing. Submitting this letter during underwriting review provides carriers with documented evidence of community-level risk reduction that can support both eligibility and premium outcomes.

Should I carry umbrella liability coverage on my Yorba Linda home?

Yes. Yorba Linda’s larger properties, pools, and frequent entertaining create above-average premises liability exposure. Standard homeowners liability limits can be exceeded by a single incident in California’s litigation environment. An umbrella policy extending coverage to $2–5 million adds that protection for $200–$400 per year, among the most cost-effective asset protection available to high-net-worth homeowners.

How do I find out if my Yorba Linda home is in a Very High Fire Hazard Severity Zone?

Check your address using the CAL FIRE zone viewer at osfm.fire.ca.gov. Yorba Linda’s city website also maintains its own FHSZ information page with the updated 2025 maps. Properties in the Very High FHSZ are required to maintain 100 feet of defensible space, meet Chapter 7A fire-resistive construction standards for new work, and disclose the designation to buyers at sale under California’s AB 38.