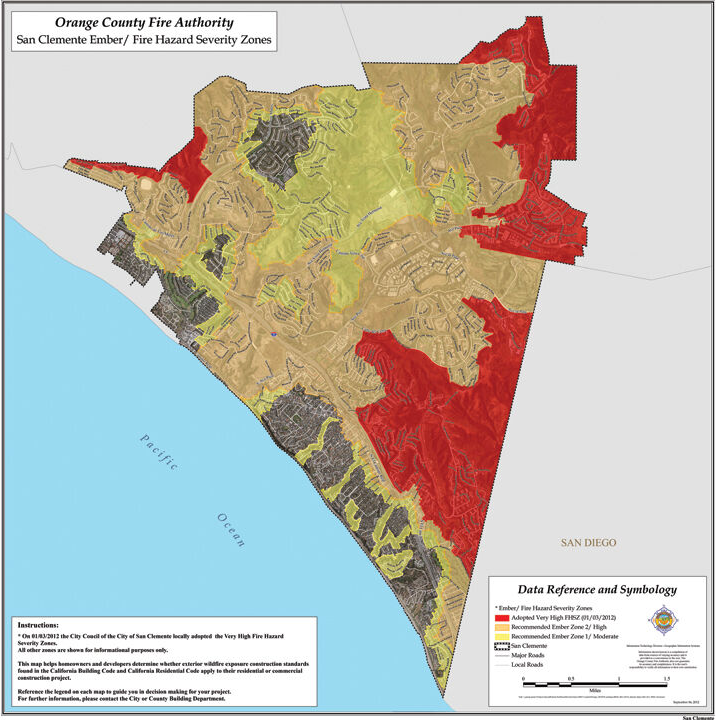

On March 24, 2025, the California Office of the State Fire Marshal redrew its fire hazard maps and placed much of San Clemente inside a Very High Fire Hazard Severity Zone.

A city known for its ocean views is now mapped for canyon fire, and homeowners insurance in San Clemente has to keep up. Old Harbor Insurance, an independent agency serving Orange County, helps homeowners account for bluff erosion, hillside movement, and wildfire exposure on a single property.

Few markets stack three distinct geological and climate risks against a single roofline the way this stretch of the South Orange County coast does. Property owners reading their declarations page against that reality often find the gaps only after a loss. Reviewing those gaps with a licensed independent agent before renewal season is one way to avoid that surprise.

A Coastline That Carries Three Risks at Once

San Clemente occupies a narrow band between the Pacific and the inland canyons, and that geography concentrates hazards. Bluff-top parcels face shoreline erosion, hillside neighborhoods sit above slow-moving slide planes, and the brush corridors flagged by CAL FIRE carry wildfire risk. A standard policy treats these as separate questions, yet one San Clemente home can be exposed to all three.

That overlap is the reason a single base policy rarely covers everything a San Clemente homeowner actually faces.

What Standard Policies Leave on the Hillsides

Earth movement is the category that catches most hillside owners off guard. According to the Insurance Information Institute, a landslide is treated as earth movement and is excluded from standard homeowners policies, the same way an earthquake is. Damage from a shifting slope, sinking foundation, or collapsing hillside generally falls outside the dwelling coverage homeowners assume protects them.

The risk is not theoretical here. The San Clemente Times reports that the Nelson Landslide along Calle Vallarta has been shifting since early 2023, leaving one home uninhabitable while its owner pays both rent and a mortgage because landslide damage is not covered.

How a Difference in Conditions Policy Fills the Gap

A Difference in Conditions (DIC) policy is the primary tool for covering perils a standard contract excludes. These policies are written by surplus lines insurers and can combine landslide, mudflow, earthquake, and flood coverage in a single contract. Because they sit outside the admitted market, access usually runs through a broker with surplus lines relationships rather than a single-company agent.

When Hillside Damage Might Still Be Covered

One exception turns on cause. The California Department of Insurance explains that under the principle of efficient proximate cause, if a covered peril such as wildfire is the primary cause of a later mudflow or debris flow, the resulting damage may be covered under a standard policy. Homeowners denied a claim on these grounds can file a request for assistance with the department.

Bluff-Front Homes Face Sharper Carrier Scrutiny

Coastal erosion adds a slower, quieter pressure on the west side of the city. Wave action and storm surge have undercut sections of the shoreline severely enough to force repeated closures of the rail line that runs below the bluffs. Erosion rarely arrives as a single event, which is part of why standard policies exclude the gradual land loss it causes.

Carriers have responded by underwriting bluff-adjacent property more cautiously. Owners and buyers increasingly encounter requests for updated geotechnical surveys before a policy or loan is approved, and some lenders now require structural engineering reports on bluff-top homes. Distance from the active bluff edge and documented mitigation can lower how an underwriter views the risk..

How Old Harbor Insurance Helps

Old Harbor approaches San Clemente coverage as a layering problem rather than a single policy. As an independent agency with access to 81 A-rated carriers, the firm can compare standard policies, place DIC coverage through surplus lines markets, and structure flood and earthquake protection separately where the property calls for it.

That breadth matters most when a captive agent can only offer one company’s appetite for coastal and hillside risk. Old Harbor’s agents also walk homeowners through how a policy responds after a loss, including how claims are handled for the perils that overlap on a single San Clemente property.

Match Your Coverage to San Clemente’s Real Risks

A San Clemente policy works best when it reflects the specific blend of bluff, hillside, and wildfire exposure your address carries. A licensed Old Harbor agent can review your current declarations page and identify where standard coverage stops. Get a quote online or contact the Old Harbor team to start that review.

Frequently Asked Questions

Does homeowners insurance in San Clemente cover flood damage?

No. Standard homeowners policies exclude flood damage, which requires a separate policy through FEMA’s National Flood Insurance Program or a private flood carrier. Homes with federally backed mortgages inside a FEMA-designated Special Flood Hazard Area are required to carry it.

Will earthquake insurance cover a landslide?

No. Earthquake and landslide are treated as separate causes of earth movement, so an earthquake policy does not automatically cover slide damage. Coverage for landslides comes through a Difference in Conditions policy instead.

Is the California FAIR Plan permanent coverage?

No. The FAIR Plan is a last-resort, named-peril option meant to be temporary while a homeowner secures coverage in the standard market. Its limits are often narrower than a full homeowners policy, which is why many owners pair it with supplemental coverage.

Does a Difference in Conditions policy replace a homeowners policy?

No. A DIC policy supplements a standard homeowners policy by adding excluded perils such as landslide, flood, and earthquake. Homeowners keep their base policy and layer the DIC coverage on top.

Can mitigation lower my premium in San Clemente?

Yes, in many cases. Defensible space, home hardening, and participation in a Firewise USA community can improve how underwriters view a fire-exposed property. Documented bluff mitigation and drainage maintenance can similarly support a more favorable review.

When is a defensible space inspection required to sell a home?

Since July 1, 2021, sellers of property in a High or Very High Fire Hazard Severity Zone must provide documentation of a compliant defensible space inspection. The requirement reaches more San Clemente properties now because of the expanded 2025 zone maps.

What should I document about my property before a coastal or hillside loss?

Keep dated photographs, any geotechnical or structural engineering reports, and records of drainage and vegetation maintenance. This documentation helps establish the cause of a loss, which often determines whether a claim falls inside or outside your coverage.